Council debates proposed sales-tax audit contract that would pay third party 45% of newly recovered revenue

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

Council members questioned a proposal to hire Azovar Audit Solutions to review local sales-tax coding and reallocate miscoded revenue to Sedro-Woolley; concerns centered on a 45% contingency fee, scope limits, and a vendor clause flagged by a public commenter.

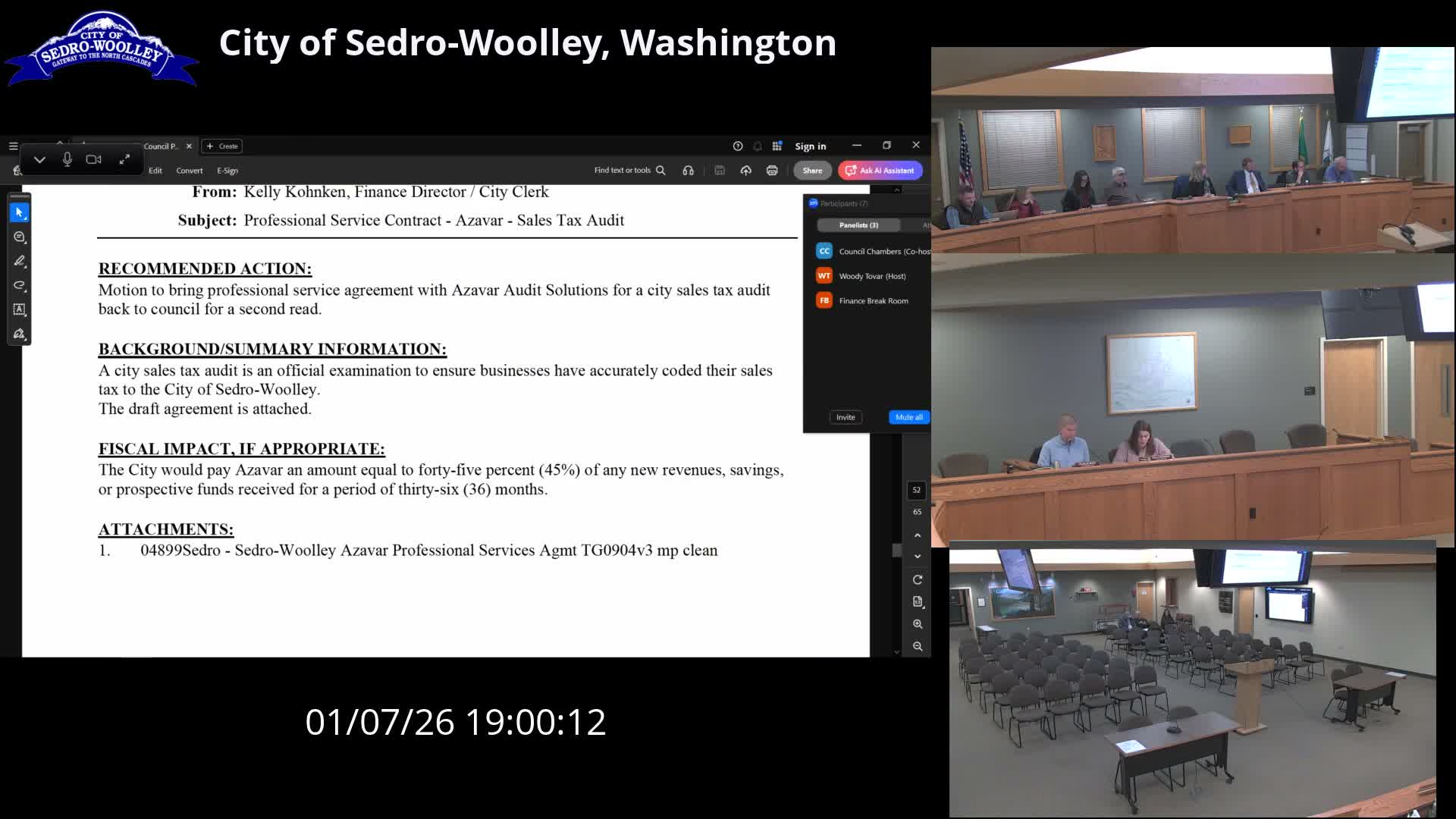

Sedro-Woolley councilmembers debated whether to advance a professional services agreement with a private firm to review the city’s sales-tax allocations. City staff described the proposal as a targeted review to identify miscategorized transactions and reassign them to the city where appropriate, not as a Department of Revenue–style forensic audit. The company is proposed to receive 45% of any newly recovered revenues for a 36-month period.

“45 is a high percentage for 3 years,” a staff speaker said while describing the contract’s fee structure. Multiple councilmembers raised similar concerns in the public discussion, arguing the contingency percentage could create perverse incentives and that outreach to local businesses or a flat-fee study might be preferable first steps. One councilmember suggested starting with Chamber of Commerce–led outreach and internal guidance to address coding errors before hiring an outside firm.

Public comment amplified those concerns. Carl DeYoung, a resident, pointed to section 1.2 of the packet and warned the contract language appears to give the vendor control over audit-related changes, saying the vendor might be allowed "to take charge of the ordinances and that the city couldn't start audits or change audit related ordinances or contracts without the vendor's written approval." DeYoung urged elected officials to retain decision authority for constituents.

Staff defended the concept as a limited, revenue-recovery arrangement: the firm would work to identify revenue that has been miscoded to other jurisdictions and assist with reallocation but would not perform Department of Revenue–level enforcement actions or levy retroactive criminal referrals. Several councilmembers asked that the item be returned for additional review; the transcript records a motion to bring the agreement back for a second reading but does not include an unambiguous final vote on advancing the contract in public session.

Next steps: Councilmembers asked staff to pursue alternatives including business outreach and to return contract language and governance clarifications (including the questioned section 1.2) for further review before any authorization.