Cheltenham SD finance committee: $30M reserve, state grant timing shifts revenue recognition; audit clean

Summary

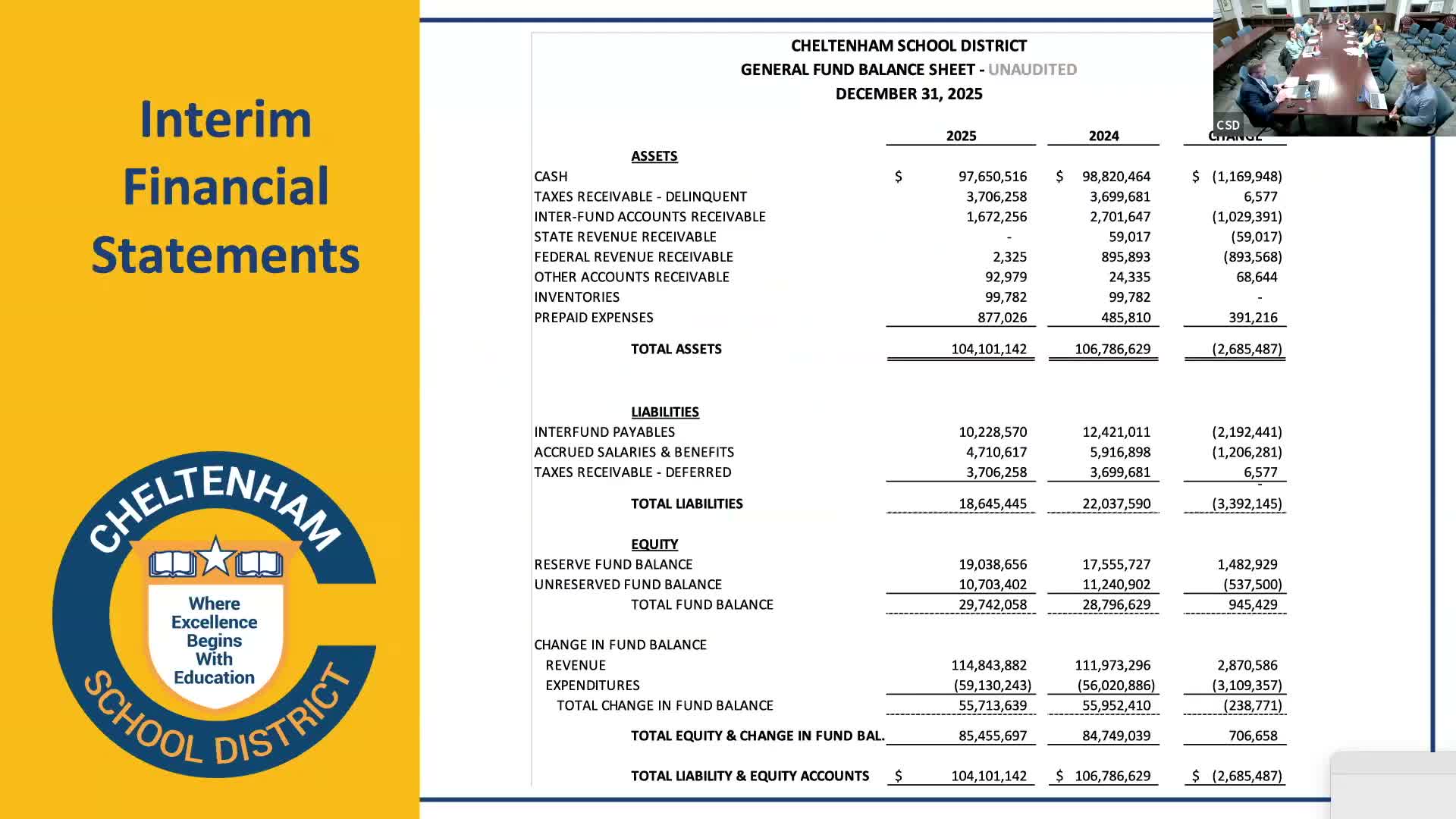

The Cheltenham School District finance committee reviewed interim statements through Dec. 31, 2025, was told the district retains a roughly $30 million reserve, learned state budget timing shifts Ready to Learn/tax-equity recognition into next year, heard a clean independent audit opinion, and placed three items on the upcoming legislative agenda.

At its regular finance committee meeting, Cheltenham School District staff told members the district remains structurally balanced with a substantial fund balance while changes in the state budget shifted the timing of two school‑aid allocations.

Presenter Mr. Swadhart led the review of interim financial statements through Dec. 31, 2025, saying the district "still have a relatively robust, fund balance of $30,000,000, in reserve." He told the committee local revenue this year is about $102,000,000, driven by higher real‑estate collections and stronger than expected investment income, while 70% of district spending is staffing and related benefits.

The discussion focused on recent state budget details that affect grant timing. Mr. Swadhart explained that the Ready to Learn foundation grant historically shown at about $340,333 was displayed differently on the state's spreadsheet (an interim presentation showed a larger combined figure). He said the state's final allocations reduced the foundation portion back to roughly $340,000 while increasing the tax‑equity allotment such that recognition of roughly $2.2 million will be deferred into the next fiscal year. "So now instead of receiving 1,100,000 this year, we have to wait till next year to recognize this $2,200,000," he said, describing options to either adopt a resolution to recognize revenue now (to offset tax‑appeal liabilities) or defer recognition and use funds to balance next year’s budget or reduce debt.

On expenditures, Mr. Swadhart noted increased costs in regular and special education driven primarily by contractual salary and benefit changes and highlighted a $1.3 million capital improvement outlay to repair the high‑school roof tied to a $1.0 million state grant application. He also said the district's retirement contribution rate decreased slightly, offsetting about $20,000, while medical‑insurance costs—driven by large claims and stop‑loss deductibles—remain the largest area of pressure.

The committee received a summary of the district's 2024 independent audit and single‑audit. Mr. Swadhart said both audits returned a clean (positive) opinion and that no material weaknesses or internal‑control violations were identified. The independent auditor is scheduled to present the full report at the February meeting.

Three board action items were placed on next week’s legislative agenda for formal consideration: re‑approval of Mr. Swadhart as treasurer for the fiscal year (a formality with no additional pay), a bond‑proceeds reimbursement resolution to allow the district to reimburse general‑fund expenditures from future bond proceeds, and the matter of hiring a construction manager for the Cedar Broken Glen Side construction project (contractors were approved previously; a construction manager has not yet been finalized). Mr. Swadhart explained SiteLogic held its prior price schedule but that the new project requires more on‑site hours than prior work.

The committee approved the December minutes by voice vote during the meeting and adjourned after a motion. Next steps: the independent auditor will present the in‑depth report in February, and the committee will begin a preliminary budget review for the 2026–27 school year as part of the Act 1 budget timeline.

Notes on sourcing and uncertainty: dollar amounts and some spreadsheet labels were described by staff in the meeting; certain figures (as quoted by staff) reflected the meeting transcript's presentation and in a few places contained inconsistent punctuation/zeros. Where the meeting record gave specific amounts, this article uses those figures and notes when staff described timing/recognition shifts rather than final cash receipts or completed board votes.