Independent audit delivers three clean opinions; GASB change reduces fund balance by about $1.4M

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

Boyer Ritter presented unmodified opinions on the district's financial statements, compliance and major federal program (Title I). Auditors flagged implementation of GASB guidance on compensated absences, increasing the reported liability and decreasing fund balance by roughly $1.4 million; no material weaknesses or noncompliance were identified.

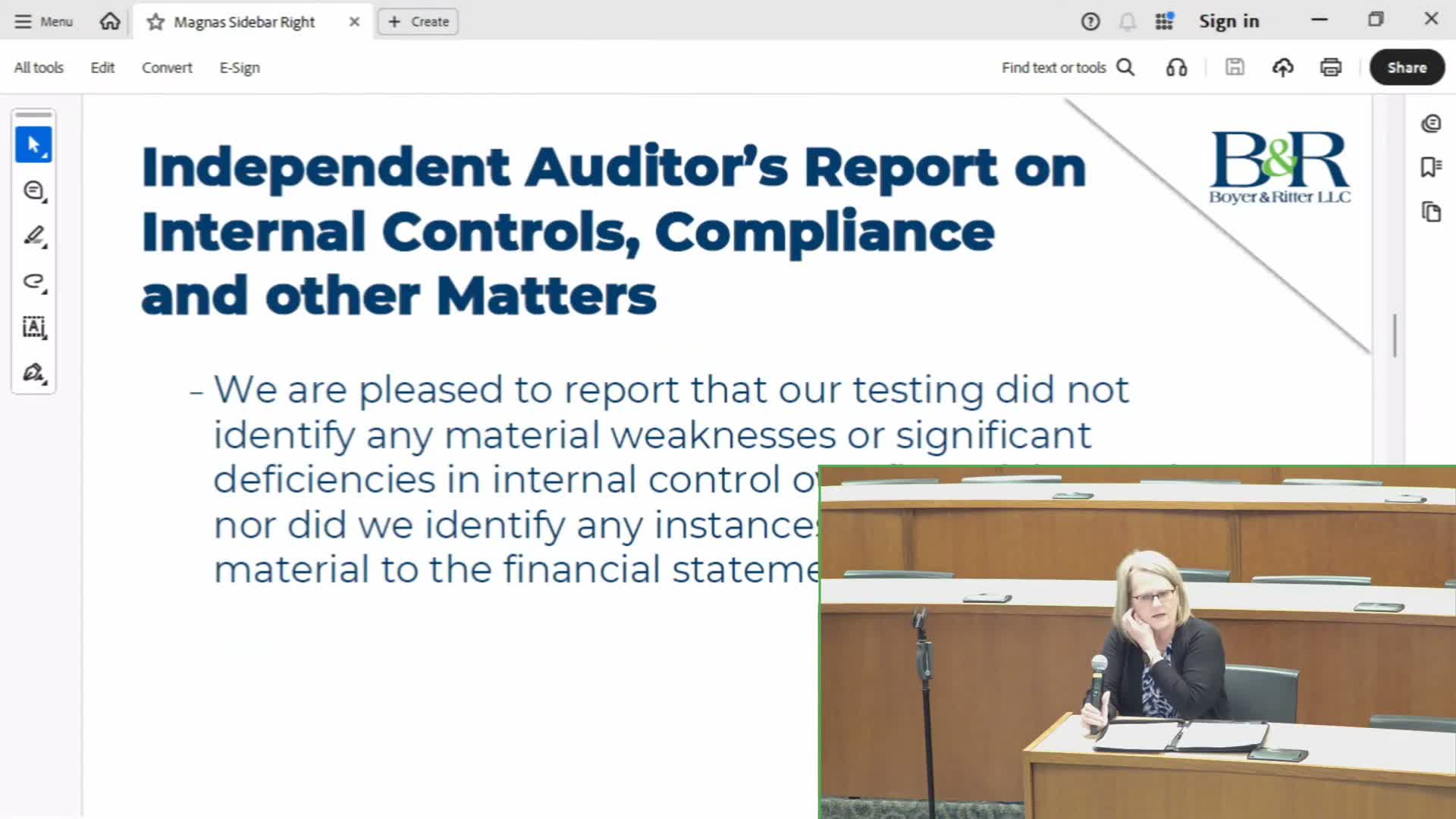

Tina Geip of Boyer Ritter presented the district’s annual financial audit and reported three clean (unmodified) opinions: the financial-statement audit, the internal-control/compliance audit and the single-audit opinion for the major federal program tested (Title I).

Geip said the district’s federal expenditures were about $5.6 million this past year and that Title I — tested as the major program — comprised approximately $1.2 million of those expenditures. The auditors found the district complied with program requirements and identified no deficiencies related to the tested federal programs.

The auditors highlighted the district’s adoption of GASB 101 for compensated absences, which required a recalculation of the liability and resulted in a restatement that lowered the reported fund balance by about $1.4 million as of June 30, 2024.

Financial highlights Geip summarized included general-fund results (revenues were about $6.7 million above budget, driven in part by higher tax collections; expenditures including transfers were about $6.8 million above budget, largely due to transfers to the capital reserve), capital-reserve ending balances (~$9.2M) and capital-projects balances that include last year’s $15M bond issue. The auditors also reviewed food-service and property-rental funds and noted no reportable findings.

Geip said auditors identified no material weaknesses or significant deficiencies and had no disagreements with management. She noted upcoming GASB 103 reporting-model changes and a federal single-audit threshold change (from $750,000 to $1,000,000) that may affect next year’s reporting.

Board members thanked the audit team for the clear presentation; no formal board action was required at the committee meeting.