Board weighs two borrowing paths for K–8 project; timeline set for bond resolution

Get AI-powered insights, summaries, and transcripts

Sign Up Free

Summary

PFM presented two financing scenarios for the district’s planned $120 million in projects: a front-loaded option that lowers lifetime cost but raises near-term debt-service to about $8.69M, and a level-payment option with a softer near-term impact but higher long-term cost. Staff briefed the board on reserves, tax-millage implications and a Feb. 19 debt-resolution timetable.

Representatives from PFM, the district’s financial-advisory firm, presented financing options for the district’s multi-step capital plan. Zach Willard, managing director, told the committee the plan supports roughly $120 million in projects, noting the district already issued a first $15 million tranche last summer and expects two roughly $45 million borrowings (spring and next year) with a final cleanup issue in 2028.

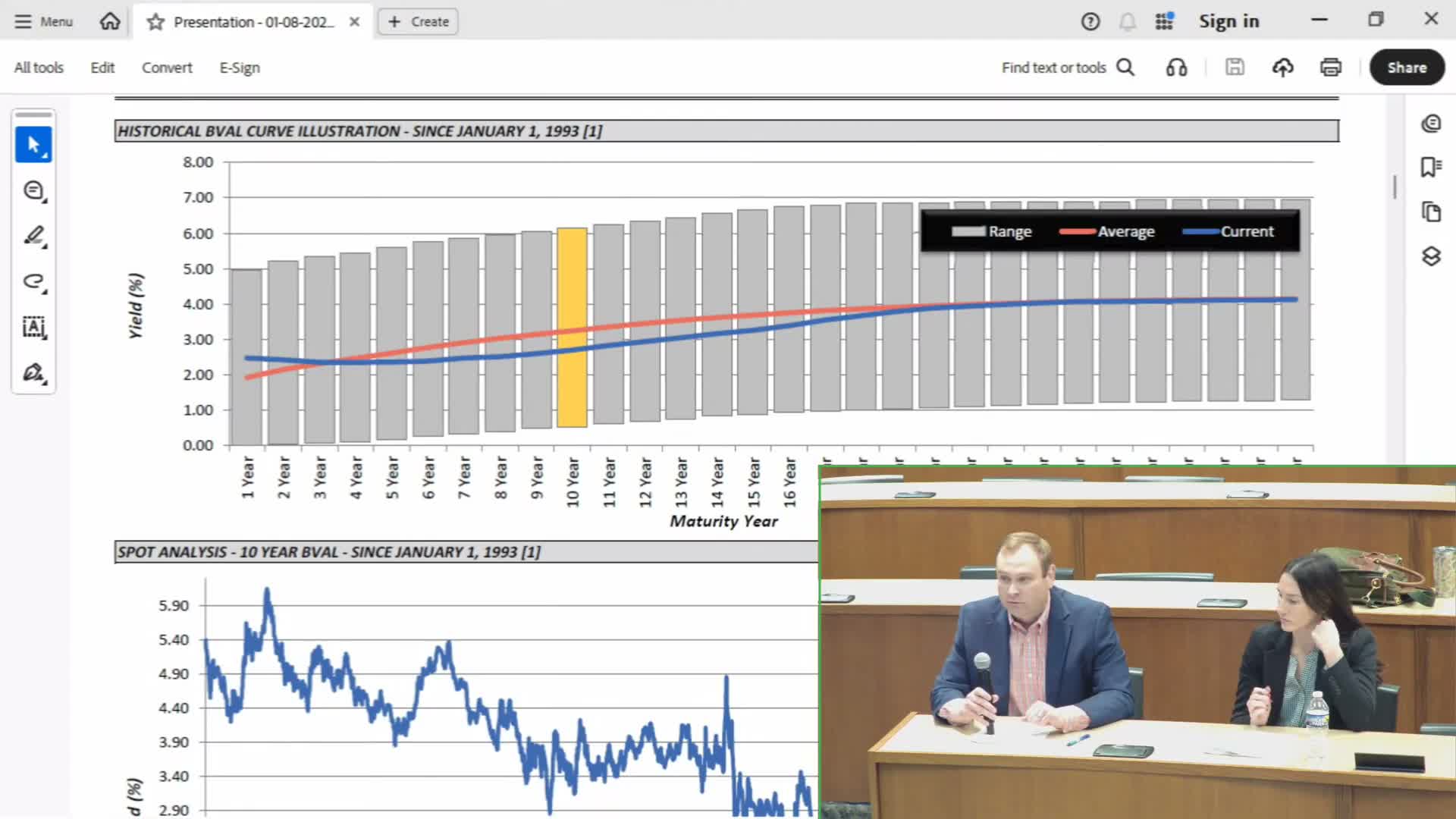

Willard framed two core scenarios. Scenario 1 front-loads principal repayments to reduce total interest over 30 years but creates a near-term debt-service peak around $8.69 million; the model shows the district would have to ramp the debt-service budget by roughly $650,000 per year for several years to reach that level. "Interest rates have come down...this is the 10-year rate that we're showing you to benchmark," Willard said, explaining why now may be an opportune time to finance.

Scenario 2 spreads payments more evenly, holding the peak near $7.3 million and requiring about $1.2 million in additional budget increases over a few years instead of the $2.5 million implied by Scenario 1; however, PFM and board discussion noted Scenario 2 increases total repayment over the life of the borrowing by an estimated ~$17 million compared with Scenario 1.

Board members asked whether the district could use capital reserves or unassigned fund balance to smooth near-term impacts. Finance staff cautioned that some reserves are one-time resources and that the recurring $647,000 shown in planning columns is a continuing obligation. Administrators and board members discussed potentially combining reserves and modest budget increases rather than an earmarked tax increase.

On timing and next steps, staff said the committee can authorize the team to proceed with analysis now but emphasized that a formal debt-resolution vote is scheduled for Feb. 19; bids were referenced in committee as arriving in late February and the board would vote on bids in March, with final issuance soon after. Staff committed to modeling a hybrid scenario (a mid-path between the two bookends) and to provide additional detail on reserve impacts before the February decision.

No binding decision or formal bond issuance occurred at the committee meeting; the board signaled clear interest in a follow-up analysis and scheduled the debt-resolution process for February.