Forensic audit flags $1.1M in Merit Academy payments as unverified; auditors seek records

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

A forensic accounting team told the Woodland Park School District board it verified roughly $4.0 million of $5.2 million paid to Merit Academy but could not verify about $1.1–$1.2 million; auditors recommended the board authorize a follow‑up review of Merit Academy records to close documentation gaps.

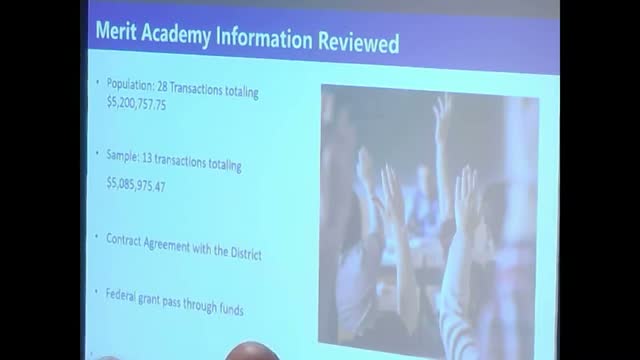

A forensic accounting team briefed the Woodland Park School District RE‑2 board on financial flows tied to Merit Academy, saying the audit traced $5.2 million in payments to the charter school but could only verify $4.0 million of that amount.

"We identified 28 payments totaling $5,200,000. Of that amount... 4,000,000 of the $5,200,000 we feel is verified," Brandon Waldron, a senior manager on the forensic team, told the board. "The $1,100,000 to $1,200,000 we do have questions on. We do not feel that we have fully verified why that money was provided."

The auditors described their scope as a risk‑based review of FY2023–24 transactions and said they tested samples of bank, credit‑card and manual journal entries. They reported control gaps across the district’s records—24 of 60 tested check payments lacked a check‑request form, several credit‑card transactions lacked itemized receipts, and some manual journal entries did not show preparer or approver information.

Why this matters: Merit Academy operates under a contract that the auditors read into the record, which requires district documentation and, for certain federal and state funds, reimbursement‑style records. The forensic team said Merit’s monthly billing often consisted of pro‑forma budgets divided by 12, with little supporting expense documentation available from the district files reviewed.

Auditors recommended a limited follow‑up: obtain Merit Academy’s financial records and supporting documentation for the questioned amounts, test additional transactions, and confirm whether funds were expended in compliance with applicable federal and state program rules. Waldron estimated the additional work could be completed for roughly $10,000 if Merit provides documents promptly; the duration would depend on how quickly Merit responds.

Board reaction and next steps: Board members said the additional effort may be warranted to restore community confidence. Several members emphasized fiscal constraint but noted that resolving the $1.1M question could clear lingering community concerns about past administrative practices. Finance staff and the auditors also noted that if the board authorizes the expanded scope, auditors would request Merit’s contracts, expense backups and communications used to calculate monthly billings.

Officials stressed the forensic audit is an independent fact‑finding exercise, not a determination of criminal liability. As Waldron told the board, "We are here to find facts... We are not judges or juries." The board has not yet voted to expand the forensic scope; staff flagged that purchases under approximately $10,000 may be administratively approved under district policy, though the board may vote if it prefers.

The board will consider whether to authorize the auditors to seek Merit Academy records and to finalize the forensic report after that review.