International changes in HR 1 prompt Vermont committee to weigh sales-factor enforcement and GILTI/FDDEI effects

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

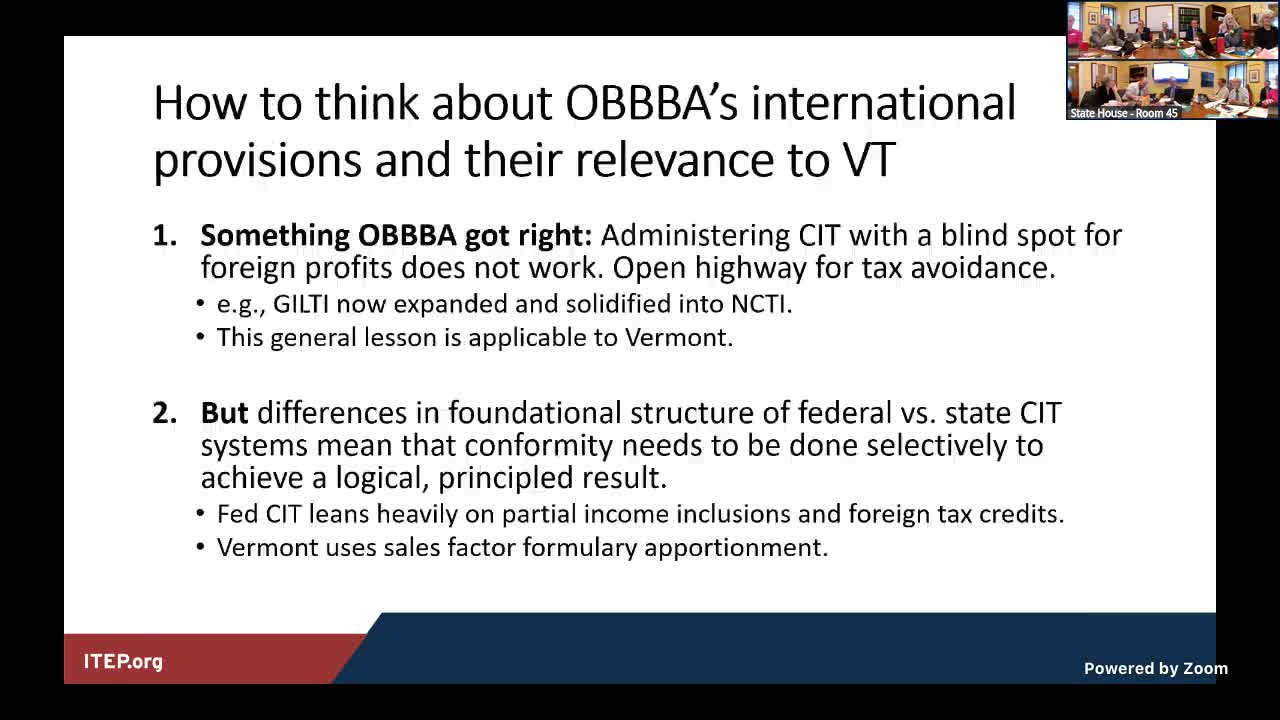

Testimony explained how federal international provisions — the foreign-derived deduction and the renamed GILTI (net CFC-tested income) — interact poorly with state sales-factor apportionment and could increase reported inclusions unless states adopt a sales-factor approach or decouple.

Carl Davis walked the committee through how international provisions in the federal code — including the foreign-derived deduction (FDDEI, pronounced by some as "FIDAY") and the successor to GILTI (now described as net CFC-tested income or NCTI) — interact with Vermont’s corporate tax system.

Davis explained that most states, including Vermont, use sales-factor formulary apportionment to tax a company's in-state share of profit based on where its customers are located. He illustrated with a simplified example: if a multinational’s worldwide sales grow, a sales-factor apportionment reduces Vermont’s fraction of its taxable income even if the company’s overall profit rises.

On FDDEI/FIDAY, Davis said the federal deduction effectively subsidizes exports by allowing roughly one‑third of export-related income to be deducted federally; states using sales-factor apportionment already avoid taxing exports and therefore may not benefit from adopting the federal deduction. "This deduction, in my opinion, does not serve a purpose at the state policy level," he said.

Davis also described the GILTI successor (NCTI), noting that the federal deduction for that category dropped from 50% to 40%, meaning a state that updates conformity dates could see the inclusion rise from 50% to 60% unless the state crafts an alternative tied to sales-factor apportionment. He recommended bringing all foreign income into the state tax base and then apportioning it by sales rather than adopting an arbitrary federal percentage.

Members raised enforcement concerns — how Vermont verifies sales claimed in foreign jurisdictions — and Davis recommended more testimony from tax administrators and multi-state enforcement groups. He emphasized that conformity choices should consider both revenue impacts and the state’s administrative capacity to audit complex, multinational filings.