Committee explores decoupling from federal business breaks (QSBS, bonus expensing) to protect state revenues

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

Witnesses warned that several federal business tax changes — notably the qualified small business stock exclusion and expanded bonus depreciation — could produce large state revenue losses and little in-state benefit; Davis urged Vermont to evaluate selective decoupling and cited other states' responses.

Carl Davis told lawmakers that certain federal business tax provisions merit serious consideration for state decoupling because the fiscal costs are large while in-state economic benefits are uncertain.

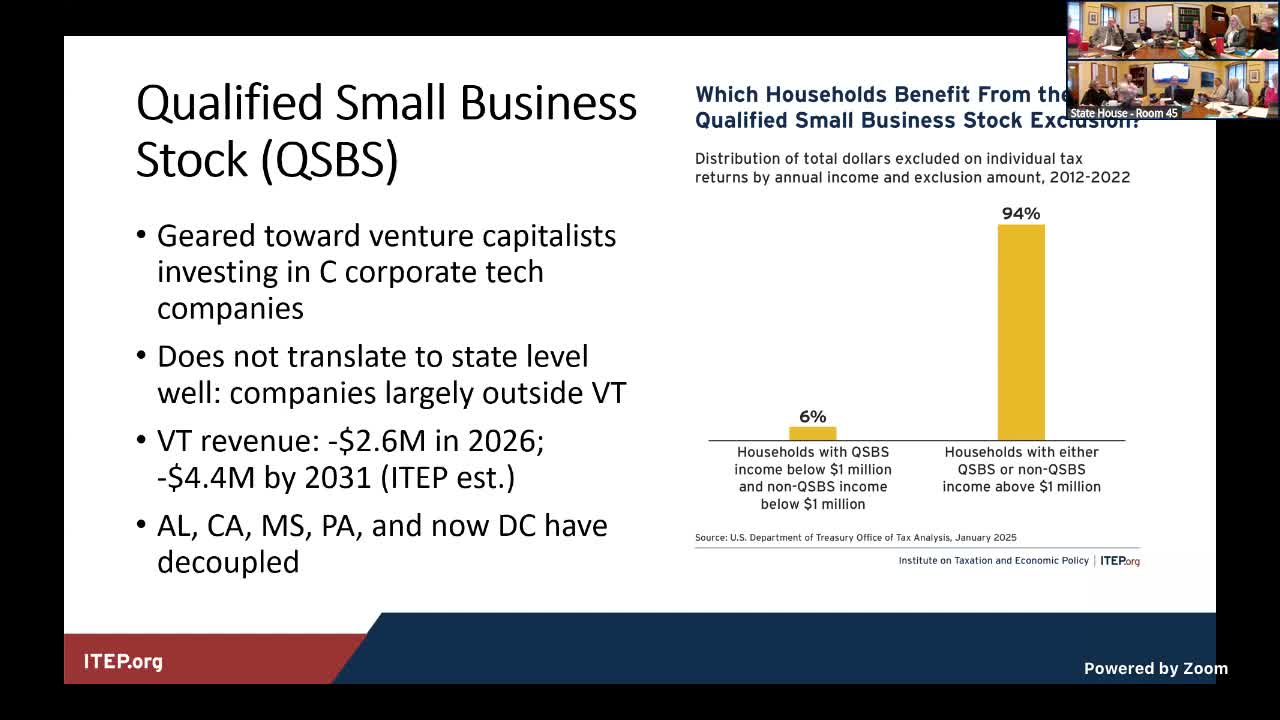

Davis described the qualified small business stock (QSBS) exclusion as "a thing that has snuck up" and said Treasury research shows it may be consuming about 2% of federal capital gains revenue. He noted that the provision historically targeted early-stage tech investors in C corporations, not the typical small businesses that predominate in Vermont, and pointed to California’s experience decoupling in an attempt to target in‑state firms (a move that faced legal and court challenges in practice).

Davis identified bonus depreciation and expanded expensing as the largest potential revenue loss from automatic conformity. "This is consistently showing up as the biggest ticket item," he said, arguing that a state that adopts aggressive expensing will subsidize investment regardless of where it occurs and may not see the intended in-state returns. He urged lawmakers to consider phased or partial decoupling and to consult fiscal analysts for multi-year revenue estimates before legislating.

Committee members asked about legal constraints on conditioning benefits to in-state investments; Davis warned of interstate commerce challenges and cited past court rulings in similar state efforts. He recommended consulting state fiscal offices and monitoring litigation in other states that have moved to decouple.

No formal vote occurred. Staff will collect fiscal office scores and legal analyses to inform any future draft legislation.