Expert tells Ways & Means HR 1 yields regressive cuts; Vermont faces choices to claw back or bolster low-income supports

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

Carl Davis (Institute on Taxation and Economic Policy) told the Vermont Ways & Means Committee that the federal HR 1 tax bill produces largely regressive benefits, with modest average gains for low-income households and outsized cuts for the highest earners; he urged the state to consider targeted responses and strengthened compliance.

Carl Davis, a tax analyst with the Institute on Taxation and Economic Policy, told the Ways & Means Committee on Jan. 15 that the newly enacted federal HR 1 produced a broad set of tax cuts that fall disproportionately on higher-income households.

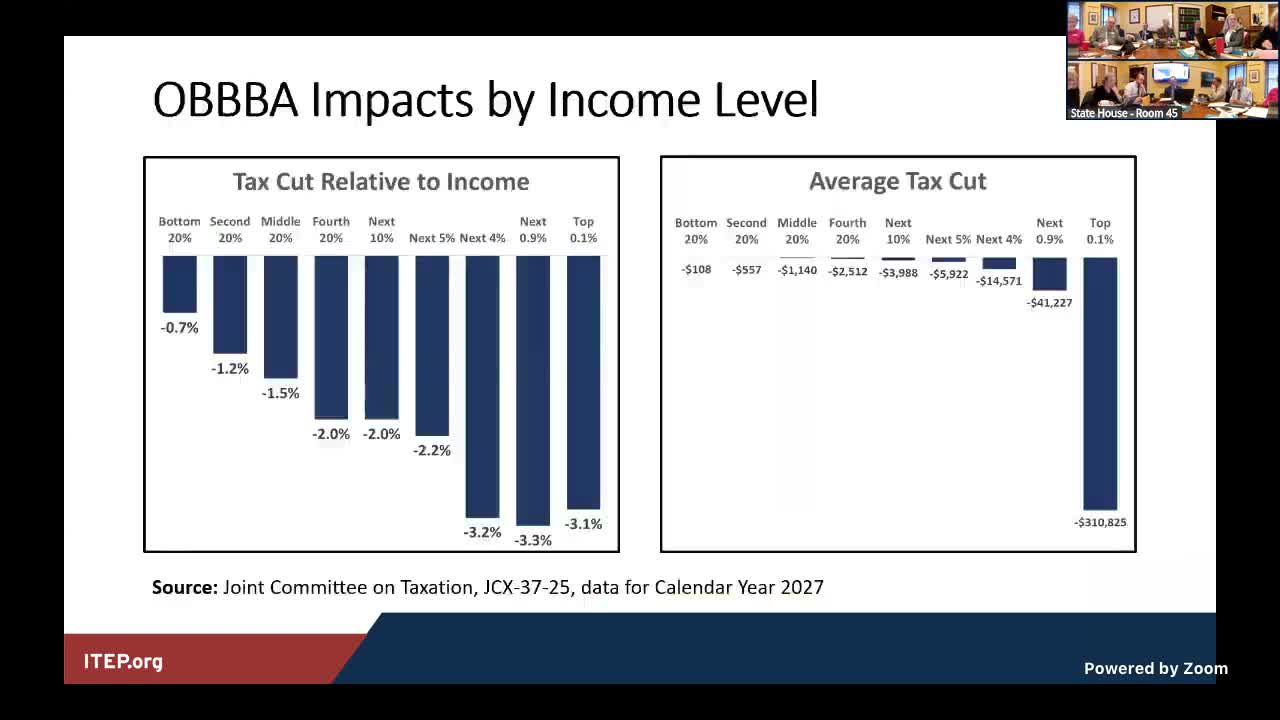

"The tax package is a regressive tax cut," Davis said, citing Joint Committee on Taxation tables and ITEP’s Vermont-specific microsimulation. He summarized the package as including rate reductions, a pass-through deduction for business income, estate tax cuts and a larger standard deduction, while noting modest average gains for low-income households.

Davis said the JCT and ITEP analyses show low-income families would see roughly $100 a year in average tax cuts from the federal package, middle-income households would see larger gains (hundreds or thousands annually), and the highest earners could receive tens of thousands of dollars a year. He estimated nationally that about half the dollar value of the bill’s tax cuts flows to households earning over roughly $360,000.

Committee members pressed for further breakdowns of income thresholds. Davis said Vermont-specific figures for the top 1 percent and top 5 percent can be provided as a follow-up and estimated the top-5 threshold nationally near $300,000.

Davis framed state options in two buckets: selective conformity and compensating state actions. He said Vermont — which moved in 2018 to couple some tax definitions to federal adjusted gross income rather than federal taxable income — should approach conformity provision by provision, picking up credits that help in-state families (for example, dependent care provisions) while declining federal carve-outs that offer limited in-state benefit. "If a state was trying to steer tax policy back in a direction that is more closely aligned with what our constituents want," he said, "it might think about, well, is there something more we could do for lower-income working class families who aren't getting a whole lot of benefit out of the federal bill?"

The committee agreed to request follow-up data, with staff noting an Emergency Board revenue estimate meeting scheduled shortly that will provide additional fiscal context. The panel also directed staff to seek further testimony from state tax administrators about enforcement gaps in light of recent IRS funding reductions.

The hearing closed with members asking for more granular modeling of who benefits and for staff to circulate the referenced JCT and ITEP reports.