Get AI Briefings, Transcripts & Alerts on Local & National Government Meetings — Forever.

PGCPS capital programs defend change-order controls, outline PMIS plan after audit

Loading...

Summary

Prince George's County Public Schools capital programs responded to an external audit before the Board of Education audit committee on Jan. 12, 2026, defending their change-order processes, citing documentation and timeliness metrics, and announcing plans to solicit a project-management information system with implementation expected in 12–18 months.

Prince George's County Public Schools capital programs leaders told the Board of Education audit committee on Jan. 12 that the district's layered contract controls and documentation reduce the risk the audit flagged and that they will pursue a project-management information system to improve transparency and recordkeeping.

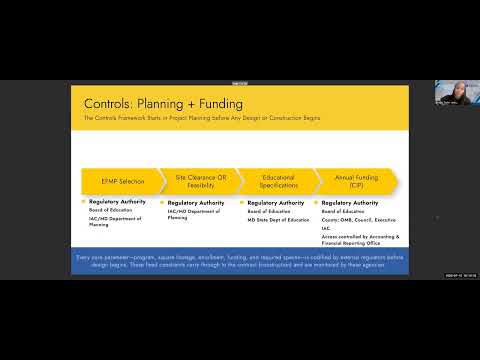

Shayla Jackson, director of capital programs, said the system of approvals begins years before construction and includes EFMP selection, mandatory feasibility studies for renovations, detailed educational specifications and multiagency design reviews. "No one office or person or department is acting alone," Jackson said, describing the multiple control gates that tie funding, scope and approvals to specific projects.

Jackson told trustees capital funding functions as reimbursement tied to a specific project appropriation rather than a lump-sum cash transfer. She described the contract lifecycle and said legal liability and the primary control point occur when a change order is executed via an AIA G701 modification and justified on a DCP Form 3,211. "If PGCPS changed to paying vendors by Apple Pay tomorrow, the contract and change order controls wouldn't change at all because the risk lives in the contract, not the payment tool for us," Jackson said.

The external audit highlighted clusters of change orders that, when aggregated across purchase orders during a 3.5-year audit period, resulted in cumulative increases above the board-approval threshold. The audit report cited 75 change orders across 15 purchase orders and noted roughly 200 change orders totaling just under $30 million across the period. Jackson disputed the implication of wrongdoing, saying most change orders had proper signatures, appeared on the board change-order log and reflected expected activity for an active construction program.

She gave examples: multiple small change orders for a "Chill and Pod" project were processed on the same days (nine change orders once totaling about $72,000; six on another date totaling about $155,000) and the district later posted linked justifications and approval documents on its change-order report. Jackson also described a New Glenridge Area Middle School sequence where a $3.9 million board-reported change order and a subsequent $139,000 modification to add solar panels were separated by calendar and system-close timing tied to board calendar and the Climate Change Action Plan adoption.

Will Smith, supervisor of capital programs, addressed whether PGCPS's change-order rate is in line with industry norms, saying construction-industry standards are "roughly 8 to 10%" and that in past audits PGCPS measured nearer 3–4% as a percentage of total work. He and Jackson noted renovation projects in older facilities commonly generate unforeseen conditions that lead to change orders, including permit inspector requirements and hidden conditions revealed during construction.

Capital programs also pushed back on procurement-related interpretations in the audit. Jackson said some procurement files were not fully attached in Oracle because the full packaged procurement records reside with the purchasing office, and she explained that paying a vendor who is not current in iSupplier can reflect documentation timing rather than an absence of procurement oversight.

On performance metrics, Jackson said the fiscal team found that "99.8% of the 4,200 invoices processed during the audit period were paid within 30 days," which exceeds the district's 97% standard; she added 95% of invoices were reviewed within three business days. The department said twelve invoices were paid outside 30 days for vendor-submission issues, vendor corrections or because approved change orders were still being entered into Oracle.

Responding to a separate audit finding that the district's PMIS was ineffective, staff said they will pursue a PMIS solicitation and an implementation partner with legacy Oracle expertise. Jackson said the department is evaluating vendors such as Kahua and Procore and expects a formal implementation solicitation and consent agenda item on the board's February meeting; she estimated 12–18 months to go live for the system and its tie-ins.

Internal audit and committee members asked for follow-up documentation on paired change orders that, when combined, could have exceeded the $250,000 board-approval threshold for a single project; Dina Thorpe, director of internal audit, asked to review the change-order analysis and staff agreed to recirculate supporting documents for further review.

The committee did not take any new formal votes on policy changes at the meeting. Staff said next steps include circulating the change-order support documents requested by internal audit, publishing a PMIS solicitation and returning with implementation details to the board.