Washington committee hears DFI overview of buy‑now‑pay‑later, data gaps and legal gray areas

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

The Department of Financial Institutions told the Consumer Protection and Business Committee BNPL products are growing rapidly but often fall outside Washington's retail‑installment law; DFI and advocates urged state data collection and targeted regulation while noting consumer risks from automatic debits and limited disclosure.

The Washington State Consumer Protection and Business Committee held a Jan. 13 work session on buy‑now‑pay‑later payment products, where the Department of Financial Institutions (DFI) described how BNPL works, the size of the market and limits to current oversight.

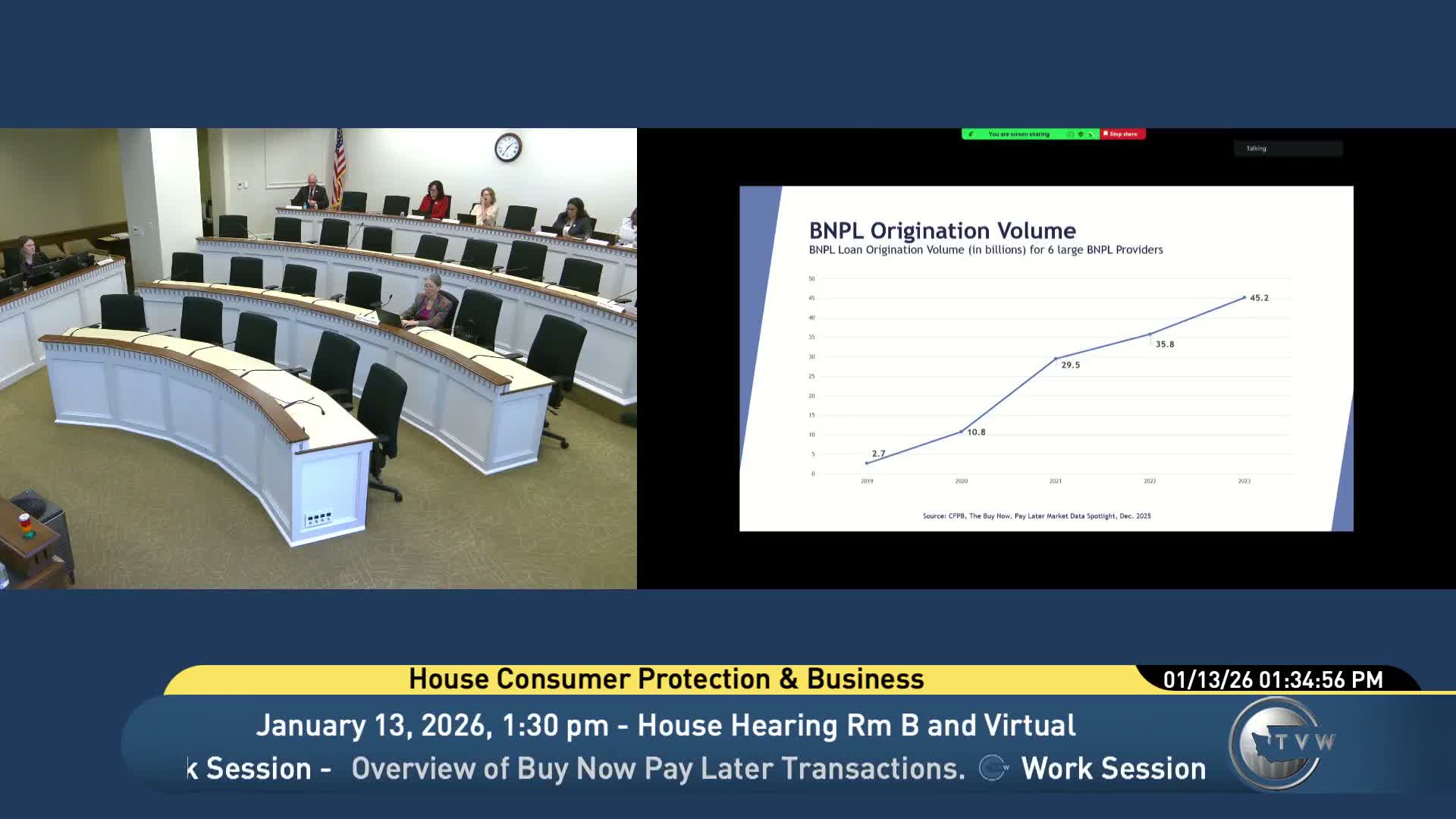

DFI policy director Drew Bowden told lawmakers BNPL typically offers four or more installments at the point of sale, usually with no interest or origination fee, automatic electronic payments and sometimes only soft credit checks. "It's a short term consumer financing product," Bowden said, noting some providers report activity to credit bureaus while others do not. He cited a CFPB data spotlight showing national BNPL volume rising from about $2.7 billion to $45.2 billion over four years and average loan amounts near $135–$150.

Why the products sometimes avoid state loan laws was a central point. Jinju "JJ" Choi of DFI explained that Washington's Retail Installment Sales of Goods and Services Act (RISA) treats transactions that either charge a service fee or require more than four installments as retail installment transactions. "Pay‑in‑4 often falls into a legal gray area," she said, because many common BNPL products have no fee and exactly four payments.

DFI officials told the committee they do not currently regulate most BNPL providers and therefore lack regulator‑collected complaint or default data, but they offered to compile more information for lawmakers. Committee members asked whether DFI could compare BNPL with earned‑wage‑access and payday products and whether BNPL automatic debits worsen household ability to pay for essentials.

Lawmakers and panelists repeatedly flagged disclosure and automatic‑debit practices as potential consumer harms. DFI noted late fees (DFI cited roughly a $7 minimum) and said the automatic payment structure can make BNPL charges effectively invisible to consumers.

The session produced no regulatory vote but lawmakers signaled plans to draft regulatory language. Chair called for continued fact‑finding so the legislature can weigh targeted state action in the absence of comprehensive federal rules.