Senate panel reviews estate-tax options; LRO models $2.5M exclusion cuts revenue about 45%

Loading...

Summary

Legislative Revenue Office economist John Hart told the Senate Finance and Revenue Committee that raising Oregon’s estate-tax exclusion to $2.5 million would, in the LRO model, reduce collections about 45% on average — and that revenue-neutral rate changes would shift the burden upward for larger estates.

John Hart, an economist with the Legislative Revenue Office, told the Senate Interim Committee on Finance and Revenue that Oregon’s estate-tax receipts are forecast to grow — from roughly $488 million today to about $850 million in six years — and that changes to exclusion amounts significantly affect revenue.

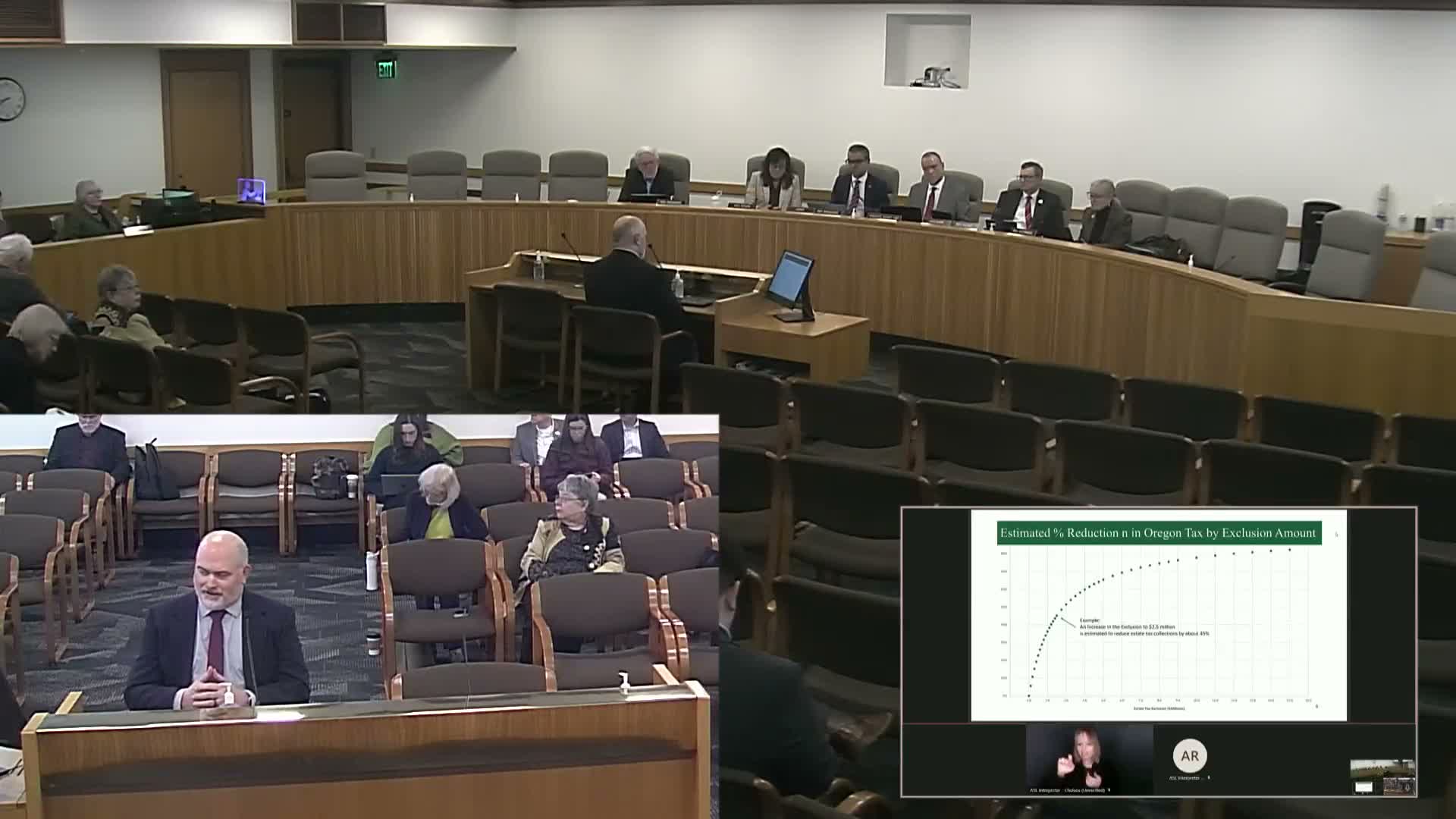

Hart showed LRO examples in which lifting the exclusion to $2.5 million would reduce estate-tax collections by about 45% on average over his five-year model. "The example this arrow points to is an increase in the exclusion to 2,500,000 under the current law structure ... estimated to reduce estate tax collections by about 45%," Hart said.

The economist cautioned that phase-in timing matters: because of due dates and possible extensions tied to dates of death, policy changes take roughly two years to fully phase in to collections. He also warned year-to-year variation can be large: the 45% figure is an average, and in any single year results may differ.

Hart presented two approaches LRO used for illustrative modeling. One keeps current rates and raises the exclusion (yielding the ~45% reduction). The second aims for revenue neutrality by increasing rates for taxable estates: Hart explained the simple math of dividing remaining tax by 55% (the post-change share) and multiplying rates (about 1.82 in his example) to approximate revenue neutrality, noting rounding and other adjustments at the top rate to keep revenue loss under 0.1%.

He also outlined a ‘‘subject-threshold’’ or cliff design: exempt estates below a taxable-subject threshold (for example, $2.5 million) but compute tax above that threshold using current-law brackets. Under LRO’s example, that design reduced revenue about 18.5% compared with current law and creates a sharp cliff where an estate just under the threshold would pay $0 while one at the threshold would pay a substantial amount.

Committee members asked whether the estate tax prompts people to relocate. Hart said relocation is one factor among many: "We know with certainty that people do move because of the estate tax, but it is part of a whole matrix of factors that people consider when they move." He also advised that indexing exemption amounts to inflation is administratively feasible but that current statute language about brackets complicates straightforward indexing.

The committee made no policy decisions during the meeting; staff said the LRO placeholder LC (LC153) will be available for the committee’s direction and study of specific policy choices.

What’s next: LRO will provide further modelling if the committee asks for specific exclusion, threshold or rate designs and for alternatives (credits, phased approaches) to mitigate cliff effects.