Norwood presenters flag $6.6 million preliminary shortfall; $750,000 regional dispatch cost added

Loading...

Summary

Town finance staff told the Budget Balancing Committee the town faces a roughly $6.6 million projected gap for fiscal 2027 and must absorb a new $750,000 regional dispatch expense; officials said revenues and state aid remain preliminary.

Speaker 5 (identified only by transcript label) presented the Town of Norwood’s preliminary fiscal 2027 budget to the Budget Balancing Committee on Jan. 14, saying the town currently projects a shortfall of about $6,600,000 and is incorporating a new $750,000 expense for regional dispatch.

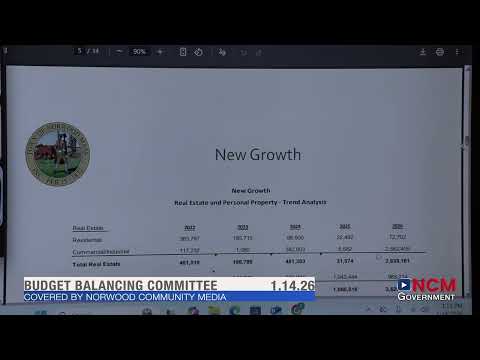

The presentation, distributed to committee members as a slide deck, walked through revenue assumptions, free cash, new growth and a five‑year forecast. Speaker 5 told the committee that certified free cash for fiscal 2026 was $24,000,008.60 and that "as of today, we have $15,352,000 of unrestricted cash." All figures, the presenter emphasized, are preliminary and subject to state Cherry Sheet and GIC (health insurance) updates.

Why it matters: the projected gap is driven by concentrated increases in several cost centers — education, public safety and health insurance — and by the requirement to include a regional dispatch cost in the general fund that the town has not previously borne. Speaker 5 said the dispatch inclusion was not a surprise but is substantial: "there's gonna be the inclusion of regional dispatch... that's a $750,000 expense in the general fund that we have not seen before."

Key figures and assumptions presented include a $3.6 million reported new growth for fiscal 2026 (roughly $2.5 million commercial/industrial and $900,000 personal property), an assumed 9% placeholder for fiscal 2027 health insurance premiums while GIC finalizes rates, and a conservative approach to local receipts (using 92.5% of three‑year averages on controllable lines). The presenter estimated total preliminary revenues of about $168.456 million before final state numbers.

Speaker 5 repeatedly cautioned against over‑reliance on high new growth continuing: "you don't wanna overestimate your new growth," they said, noting the town models a lower continued-growth figure in longer-term forecasts. The five‑year outlook presented showed revenues growing modestly while expenditures continue to outpace them, producing the structural deficit described by the presenter.

Officials answered committee questions about restricted capital funds related to the Coakley building project, with Speaker 5 saying that the excess funds (estimated in discussion as roughly $8 million to $10 million) are in the bank but restricted by IRS arbitrage rules and likely limited to capital uses rather than operating offsets.

Next steps: the committee scheduled a follow‑up meeting for Feb. 11 to revisit numbers once Cherry Sheet and additional insurance information are available. A motion to adjourn that concluded the Jan. 14 meeting was moved and seconded and carried by voice confirmation of members present.

The budget figures discussed are preliminary; the town is awaiting final state Cherry Sheet aid numbers and GIC insurance rates before adopting firm estimates.