Get Full Government Meeting Transcripts, Videos, & Alerts Forever!

Oak Harbor explains new local B&O tax, says revenue will fund marina improvements

Summary

The City of Oak Harbor Finance Department presented operational guidance on the new local business and occupation (B&O) gross-receipts tax, effective Oct. 1, 2025, detailing who must file, filing schedules, thresholds ($1,000,000 quarterly; $4,000,000 annual), exemptions, penalties, and how to request active nonreporting status.

The City of Oak Harbor Finance Department on Jan. 1, 2026, outlined how the city’s new local business and occupation (B&O) gross-receipts tax works and who must comply. The tax, the department said, went into effect Oct. 1, 2025, and the city will use the revenue to fund improvements at the municipal marina.

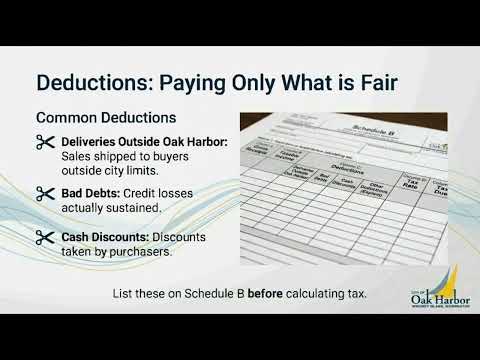

The guidance explained the tax is assessed on gross receipts — the total revenue or value of products sold within city limits before expenses are deducted — and applies only to activity conducted in Oak Harbor. "Unlike an income tax..., the B&O tax is a gross receipts tax," the presenter said, adding that state B&O and sales-tax collections remain separate.

Why it matters: the city set high filing thresholds to limit burden on small businesses. The finance department said businesses with quarterly gross receipts below $1,000,000 (or $4,000,000 on an annual filing basis) owe $0 in B&O tax, and estimated roughly 1% of local businesses will pay under current economic data. Still,…

Already have an account? Log in

Subscribe to keep reading

Unlock the rest of this article — and every article on Citizen Portal.

- Unlimited articles

- AI-powered breakdowns of topics, speakers, decisions, and budgets

- Instant alerts when your location has a new meeting

- Follow topics and more locations

- 1,000 AI Insights / month, plus AI Chat