Senate Agriculture Committee reviews omnibus agriculture bill with changes to municipal regulation, farm kitchens, taxes and siting rules

Get AI-powered insights, summaries, and transcripts

Sign Up Free

Summary

Legislative counsel walked the Senate Agriculture Committee through a lengthy miscellaneous agriculture bill that would: clarify municipal limits on regulating farming, raise thresholds for required agricultural practices, set a $250,000 accessory‑business permit threshold, add a $75 farm‑kitchen license, move the Vermont Agricultural Credit Program under VEDA, and add tax and energy‑siting provisions; the committee plans to vote on the draft tomorrow.

Legislative counsel Rodney Shaw walked members of the Senate Agriculture Committee through a draft miscellaneous agriculture bill that would make broad changes across municipal regulation, farm licensing, tax treatment for small farm income and energy siting.

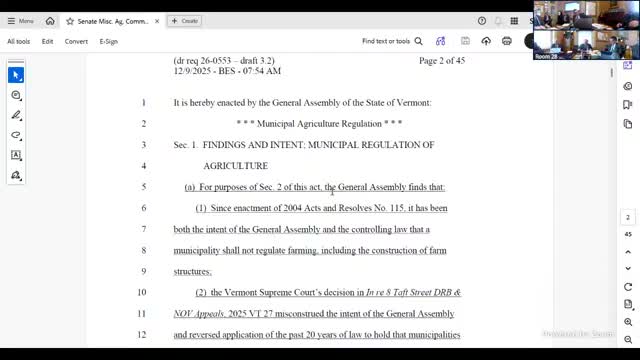

Shaw said the first three sections are intended to overturn or clarify a Vermont Supreme Court decision related to municipal authority, restoring a general rule that "a municipality shall not regulate farming, including the construction of farm structures," and adding legislative findings to that effect. He said the Agency of Agriculture, Food and Markets drafted language that would not only reinstate the prior status quo but also expand the list of activities municipalities could not by bylaw regulate, including cultivation, grazing and small backyard poultry (excluding roosters).

"These sections are meant to undo the holding of Task Street," Shaw said, explaining the changes were designed to prevent unexpected municipal bylaws from regulating ordinary farm practices. He added that the bill ties the limits on municipal regulation to whether an operation meets the statutory minimum thresholds and the required agricultural practices rule.

The draft would also change several thresholds and reporting rules. Among the measures described, the bill would raise the gross‑income threshold that triggers required agricultural practices from $2,000 to $5,000 and would permit some regulation of smaller acreage (1–4 acres) where sufficient land base exists for nutrient and waste management, an expansion from an earlier 4‑acre threshold. Shaw said the accessory on‑farm business permit tests would change from a percentage‑of‑sales test to a hard dollar threshold so that structures used for storage or sale of qualifying on‑farm processed products would not require a permit if those products do not exceed $250,000 in sales.

Tax proposals discussed by Kirby Keegan, legislative counsel on the tax portfolio, include excluding net farm profit up to $10,000 from Vermont taxable income so that incidental or hobby farm receipts would not be reported, and a targeted capital‑gain exclusion for sales of farm real estate when the buyer continues farming and is related to the seller or a long‑time employee. Keegan cautioned the capital‑gain provision contains a clawback if land is later developed and that the draft raises significant compliance and administrative issues. "If you don't have more than $10,000, you would not report that and that income would not be taxed," Keegan said of the net‑profit exclusion.

The bill also would expand the farm‑to‑school program to authorize the Agency of Agriculture to use contracts as well as grants to support school programs, and would revive related administrative provisions such as adjustments to seed labeling, reporting of genetically engineered and pesticide‑treated seeds, and new registration and reporting language.

Katie McLennan, who reviewed the farm kitchen language, said the draft creates a new "farm kitchen operation" classification in the health chapter and adds it to the list of food‑manufacturing establishments; the bill proposes a $75 license fee for farm kitchen operations. "A farm kitchen operation means an accessory on‑farm business ... for preparing, preserving, packaging, labeling, or storing food products derived from crops, livestock, or other agricultural goods grown or raised on the farm for farm direct sales, donation, or distribution," McLennan said.

Shaw described energy‑siting provisions that would require applicants for certificates of public good to include data on primary and secondary agricultural soils and to fund a cradle‑to‑grave carbon audit that accounts for manufacturing, transportation, deployment and disposal of technologies such as solar panels and batteries and for 25 years of foregone agricultural production.

Other items include moving the Vermont Agricultural Credit Program into the Vermont Economic Development Authority (VEDA) statutory chapter while keeping loan‑eligibility standards unchanged, removing a $2,500 fee for large farm operations and a $1,500 fee for medium operations (loss of fee revenue roughly estimated at $230,000), and a proposed stakeholder study — to be convened by the Agency of Natural Resources with the Agency of Agriculture — to examine permitting for installing floor drains that handle processed wastewater in on‑farm facilities.

Committee members raised compliance concerns about tax and transfer exemptions tied to continued farm use and asked whether mechanisms such as liens or title‑search triggers could be used to detect later development and enforce clawbacks. Keegan recommended discussing enforcement options with the Department of Taxes and suggested alternatives such as a tax credit paired with a later penalty similar to existing programs.

No formal amendments or votes were taken; committee leaders asked stakeholders with competing interests to provide testimony and indicated they would take a formal committee vote on the draft the following day.