Comptroller: Federal Tax Law Changes, Decoupling and SALT Shift State Revenue Timing and Forecasts

Get AI-powered insights, summaries, and transcripts

Sign Up Free

Summary

Maryland Comptroller Brooke Lierman and revenue analysts told the Ways and Means Committee that the office temporarily decoupled from certain federal changes for tax year 2025, blunting an estimated near-term revenue hit while longer-term effects on corporate income tax remain uncertain.

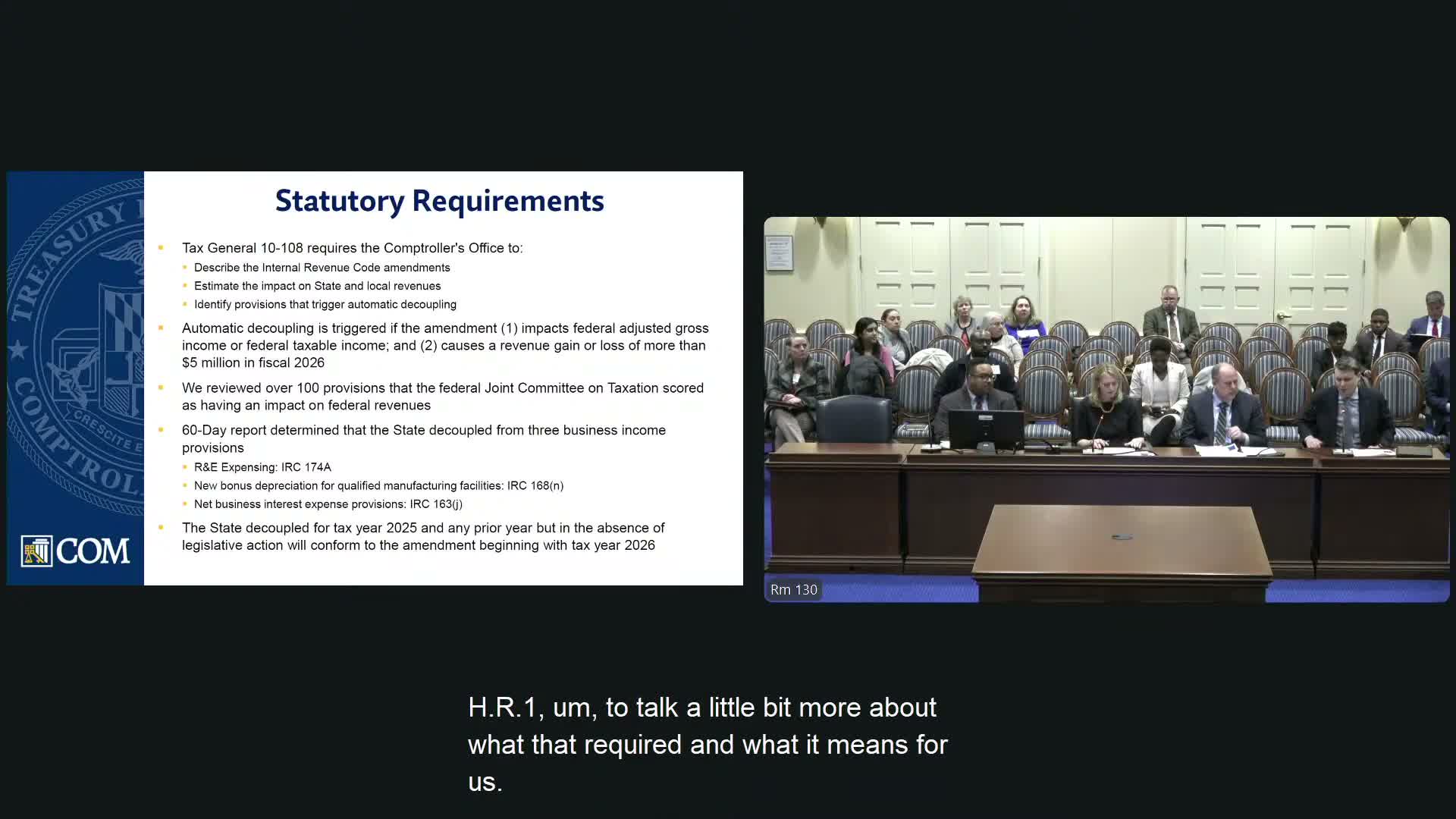

Maryland Comptroller Brooke Lierman and the Bureau of Revenue Estimates briefed the Ways and Means Committee on the fiscal effects of recent federal tax legislation, the office's statutory duties under Tax-General §10-108 and implications for the state budget.

“we determined the state temporarily decouples for tax year '25 and any earlier tax year,” Robert Rearman, director of the Bureau of Revenue Estimates, told delegates, describing the office's assessment of the federal bill’s business-income provisions. Rearman said that, under the law the comptroller uses to assess Internal Revenue Code amendments, the temporary decoupling “blunted the impact” of the federal changes on state revenues.

Rear-man told the committee that, absent the temporary decoupling, staff would have written down revenues by roughly $200,000,000 in fiscal 2026. He described a complicated fiscal picture tied to the Tax Cuts and Jobs Act and to the new federal legislation: some corporate provisions accelerate deductions, compressing state revenues in the near term (he said corporate impacts concentrate in 2027–28) while some personal-income provisions are expected to produce modest revenue gains in the out years.

Analysts outlined two elements driving short-term change: alterations to the SALT (state and local tax) treatment — described as an increase in a federal SALT cap from $10,000 to $40,000 that phases down and then reverts — and changes to business rules such as R&E (research and experimental) expense treatment and bonus depreciation. Rearman said the SALT changes and withholding-table timing may generate larger federal refunds and shift revenue timing into later parts of fiscal years, complicating near-term monitoring.

The bureau also reported early evidence of broad weakness among corporate income tax payments from top filers; Rearman said revenue from the top 500 taxpayers was down about 10 percent through the first quarter and proposed three explanations: firms adjusting estimated payments because of uncertainty, other federal provisions negatively affecting state taxes (notably international provisions), or a Maryland-specific driver. He noted defense contractors have held up while non-defense contractors showed weakness.

Committee members asked about distributional effects and drafting choices. Delegate Buckle pressed staff on concentration numbers and the effect of the federal standard deduction change on state revenues; Rearman confirmed high concentration at the top of the tax base and agreed that the interaction of federal standard deduction increases and Maryland itemizing rules helps explain some near-term state gains. Rearman cautioned that forecast accuracy is challenged by retroactive federal changes and that the office has already made proactive forecast adjustments.

The briefing closed with staff pledging follow-up data when delegates requested more granular numbers and with a reminder that permanent conformity decisions remain a policy choice for the legislature. The committee will continue fiscal briefings next week with additional state budget analysis from DLS.