State Investment Board tells Ways and Means it manages roughly $230 billion and uses ESG tools while citing fiduciary limits

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

Washington State Investment Board officials told the Senate Ways and Means Committee that SIB manages about $230 billion, primarily in pension funds, relies heavily on passive index vehicles to control fees, and integrates ESG considerations through proxy voting and stewardship while warning that imposed divestment mandates could raise costs.

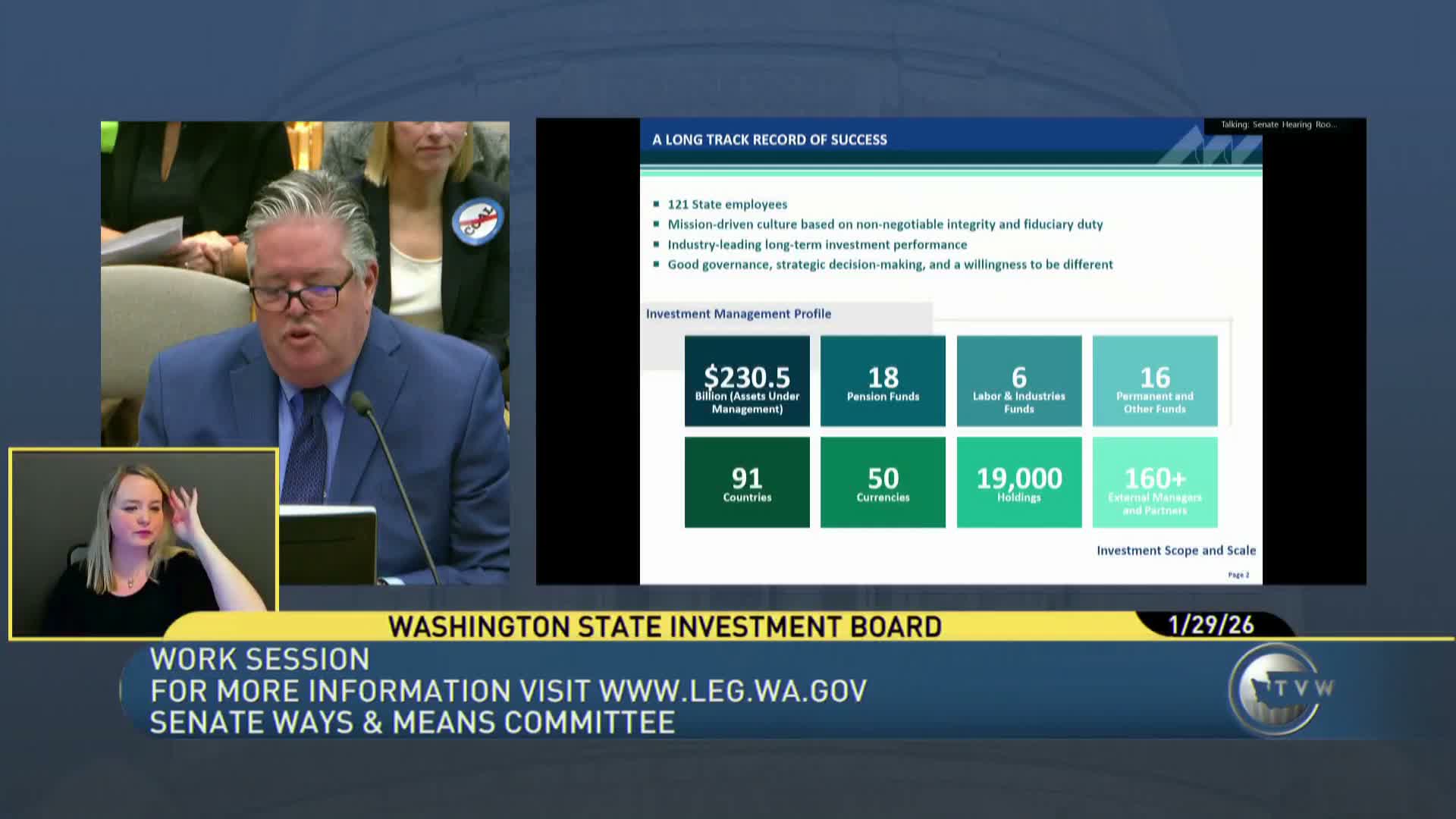

David Schumacher and James Aber of the State Investment Board told the Washington Senate Ways and Means Committee on Jan. 29 that the board manages roughly $230,000,000,000 in public funds and has a statutory duty to “establish investment policies and procedures designed exclusively to maximize returns at a prudent level of risk.” Schumacher described the portfolio mix — public and private equity, fixed income, real estate, tangible assets and “innovation” investments — and noted the commingled trust fund holds about $185,000,000,000 of that total.

Schumacher said the board structure includes 15 members (two legislators, the state treasurer, agency directors and representatives of public-employee pension systems) plus five nonvoting investment professionals. He emphasized the board sets asset-allocation policy and that much of SIB’s public-equity exposure is held in passive index products because “that keeps the costs down” and provides broad diversification. “If we were to pick and choose … it would cost more,” Schumacher said.

James Aber, director of institutional relations at the WSIB, described the agency’s sustainability and stewardship work, noting SIB adopted a formal sustainability investment belief in 2014 and rolled out climate and DEI blueprints in 2022. Aber said SIB pursues ESG integration through a materiality lens — asking whether environmental, social or governance factors will have a measurable effect on returns — and primarily uses proxy voting and engagement as tools. “We’re looking through an investment lens, not a values or ethics lens,” he said, adding that shareholder proposals on transition planning or reporting for high‑emitting companies often receive SIB support.

Committee members pressed staff on the feasibility and cost of carve‑outs or custom exclusionary mandates that would remove individual companies or sectors from index exposures. Schumacher warned such customization could add materially to fees, perhaps “tens of millions” of dollars annually, and could reduce diversification benefits. He and Aber also described possible choices short of wholesale exclusion, including social‑investment options on the defined‑contribution side and selectively using responsible passive vehicles where available.

The presentation included historical return numbers: Schumacher noted a very strong return in 2021 of 28.7 percent, while long‑term averages were closer to 8–10 percent depending on the timeframe. He framed investment choices as multi‑decade decisions tied to beneficiaries’ retirement horizons, not short‑term budget balancing. The officials repeatedly referenced the board’s fiduciary duty under state law and the legal requirement that policy changes come from the legislature if it chooses.

The committee used the session to get context ahead of public hearings later in the meeting on several bills that would constrain or direct SIB’s investment choices.