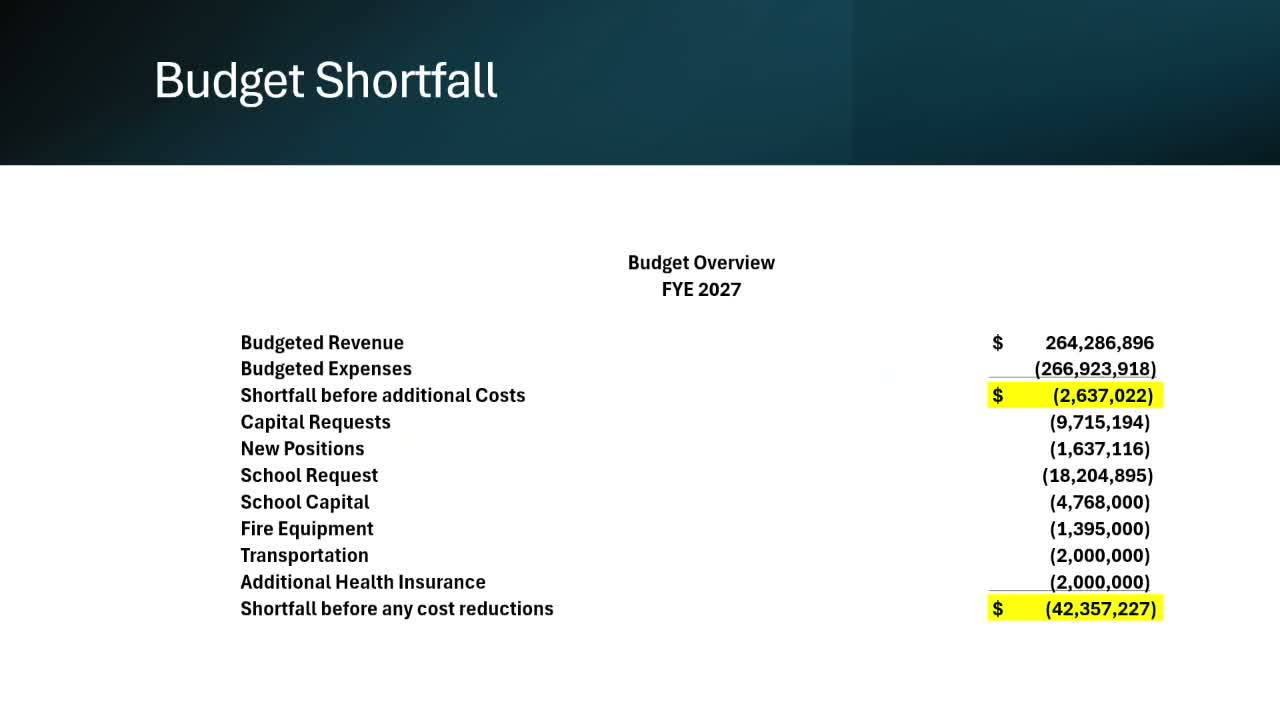

Frederick County officials outline $42 million shortfall and ask staff to draft sales‑tax referendum resolution

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

County staff told supervisors the FY27 budget exercise shows an approximate $42 million gap; the board directed staff to prepare a draft resolution to pursue a possible 1¢ local sales‑tax referendum if state legislation permits, and agreed to follow‑up workshops to refine options.

County staff told the Frederick County Board of Supervisors on Feb. 2 that the county faces a significant fiscal gap approaching $42,000,000 in the FY27 budget exercise and outlined a set of revenue and cost options to narrow it.

“Your shortfall is $42,000,000,” the county administrator said, presenting a model that combined school requests, county capital needs and operating increases. The administrator said the exercise was intended to show the “magnitude” of the challenge and described the year as an almost “reset year” requiring both short‑term and long‑term choices.

The board discussed multiple revenue levers recommended by staff, including modest increases in real property and personal property tax rates, changes to the lodging (tourism) tax and a proposed 1¢ local sales tax. Staff estimated a 1¢ sales tax would generate roughly $24,000,000 for the county if state law allows jurisdictions to adopt it for local purposes; that revenue figure drove much of the board’s attention during the meeting.

Board members voiced support for moving quickly to preserve the option. One supervisor urged staff to be ready because the legislative window is short, and the board agreed staff should prepare a draft resolution so the county could act promptly if the General Assembly’s legislation advanced. “What will do is then get a draft resolution. Get that all up ready to go just in case that happens so you don't miss November,” a supervisor said while discussing timing and referendum constraints.

Staff emphasized legal limits under Virginia’s structure—repeatedly referenced during the meeting as the Dillon Rule—and the need for additional research on the feasibility and costs of specific revenue measures. On cigarette taxes, staff presented a range of examples and cautioned the board that results vary across jurisdictions; Shenandoah County’s first year at a 40¢ cigarette tax produced under $100,000, underscoring uncertainty in projecting tobacco revenue.

Supervisors also discussed the consequences of using capital reserves to bridge operating shortfalls and were cautioned by finance staff that drawing down capital or reserves can create future fiscal strain and harm bond ratings. Staff noted the county’s reserve‑policy target (17% of general fund, roughly $49,000,000) as an important benchmark for financial prudence.

The board asked staff to prepare the draft referendum resolution, compile clearer fiscal scenarios (including what a 1¢ sales tax would buy or how it would affect debt service and school financing), and circulate follow‑up materials and spreadsheets. Staff also committed to scheduling workshops to refine assumptions and to present alternatives the board could act on in coming weeks.

Next steps: staff will deliver the draft resolution and updated fiscal scenarios for board review and hold additional budget workshops (TDR, joint EDA, public safety and a possible Feb. 18 budget workshop) to refine recommendations before any formal vote.