Witnesses tell committee TRS funded ratio remains below 80% amid assumption changes, pay raises and past retiree COLAs

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

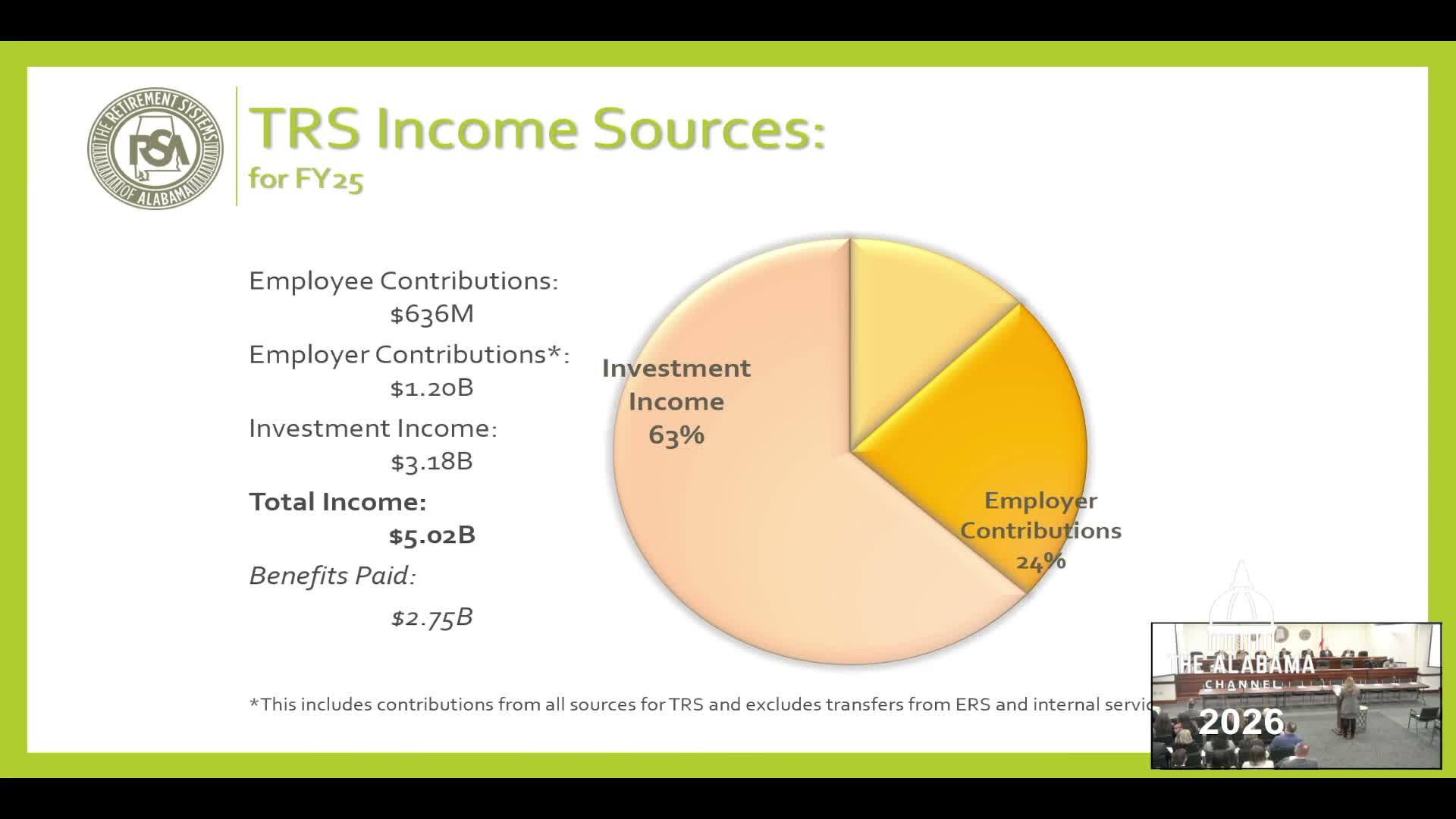

Retirement Systems testimony flagged TRS funded ratio at about 66% in the latest actuarial valuation and attributed the decline to lower assumed returns, retiree COLAs granted in the 2000s, wage increases and GASB accounting changes, with committee members asking for asset/liability breakdowns.

Representatives from the Retirement Systems explained to committee members that the Teachers’ Retirement System (TRS) funded ratio has fallen from near 100% in 2000 to roughly 66% in the most recent actuarial valuation.

The witness explained the funded ratio measures actuarially determined liabilities against assets and that multiple factors have increased measured liabilities: actuarial assumption changes (notably a lower assumed rate of return), previously granted retiree cost‑of‑living adjustments (COLAs) that were not prefunded, and recent pay raises that increase future benefit obligations. “The funded ratio is the comparison of the actuarially determined liabilities to the assets you have to offset it,” the presenter said.

Committee members asked for numerical context. A system representative said RSA total assets are about $50 billion (citation given during the hearing) and noted liabilities are materially larger, producing the lower funded ratio. Witnesses cautioned that actuarial assumption changes can be a prudent, conservative step even though they raise the calculated unfunded liability in the short term.

The committee did not vote on any TRS action during this hearing. Members asked for additional breakout data on liabilities and assets and discussed the effects of historic retiree COLAs and GASB accounting changes on the funded ratio.