Fair Plan’s rapid growth, reinsurance gaps and new financing tools spotlight market strain

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

At a California State Assembly Insurance Committee oversight hearing, Fair Plan officials described rapid policy growth, large wildfire exposure and recent reinsurance and financing moves — including a ventilated $7.1 billion reinsurance tower, a $750 million catastrophe bond, and a $600 million line of credit — as central to the Plan’s effort to avoid industry assessments.

The California Fair Plan told the Assembly Insurance Committee on Thursday that it is expanding rapidly and faces significant catastrophe-financing and rate challenges that affect the entire property-insurance market.

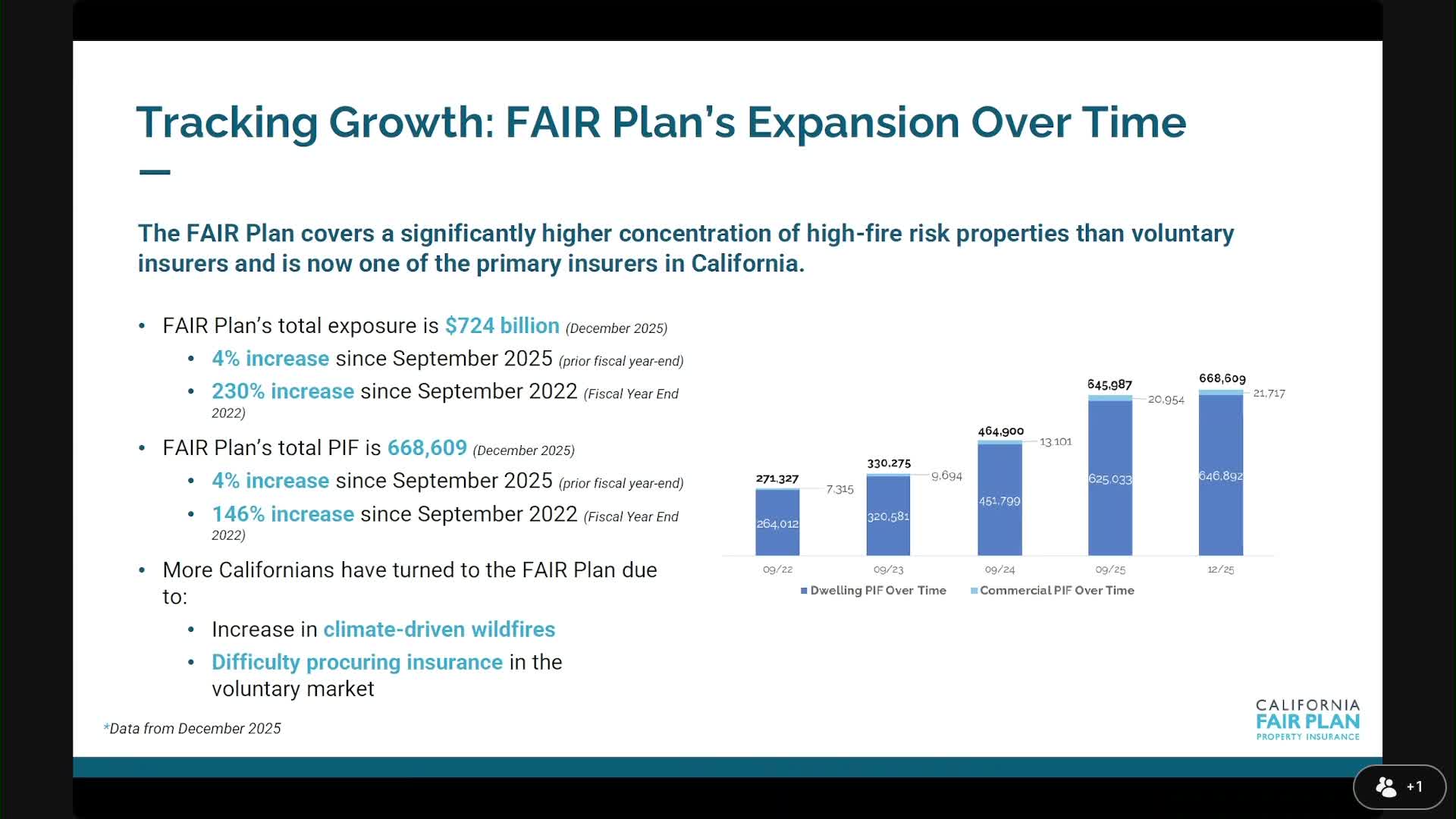

Victoria Roach, president of the California Fair Plan, told lawmakers the Plan’s exposure is roughly $724 billion and its book includes just over 668,000 policies. She said the Plan wrote about 49,000 new policies in the first fiscal quarter after the 2025 fires and that growth has slowed but remains high.

Roach described the Plan’s existing reinsurance structure as a ventilated tower arranged on 03/01/2025 with roughly $7.1 billion of capacity. The arrangement requires the Plan to exhaust a $1.25 billion retention before reinsurance pays; multiple smaller loss events that do not reach that retention would leave the Plan reliant on available cash or trigger an assessment of admitted carriers, she said. To add capacity the Plan placed a $750 million catastrophe bond that would pay out if collective losses reach about $6 billion and plans another bond in a lower layer to further fill the tower.

The Plan said it secured a $600 million line of credit authorized by recent legislation (AB226) to help with short-term cash flow and is exploring turning that into a revolving facility. Roach said those steps are intended to reduce the risk of a statutory assessment on admitted carriers in the event of large wildfire losses.

The Fair Plan also summarized recent rate filings. Using updated reinsurance-cost and catastrophe-modeling inputs, the Plan filed a company-wide average rate need it described as about 35.8 percent; previous filings in 2020–2023 showed larger theoretical needs that were approved at lower percentages. Roach said getting actuarially sound rates is critical to the Plan’s ability to shore up capital and to consider raising policy limits.

Industry groups that testified in the hearing said the Fair Plan’s lower effective rates in some ZIP codes have made it difficult for admitted carriers to depopulate the Fair Plan’s book. "You cannot depopulate the Fair Plan when somebody can go to the Fair Plan and maintain the policy for 30, 40 years because it is cheaper," Mark Sechna of the American Property Casualty Insurance Association said.

The hearing produced no committee votes. The next procedures described at the panel’s close were continued oversight, follow-up questions from members, and further engagement between the Fair Plan and the Department of Insurance (CDI).