League members push feedback on SB97 as property‑tax changes surface

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

League presenters briefed members on SB97 and related property‑tax proposals including a 5% cap, a raised new‑growth exclusion (100%→200%), and a proposal to lower city fund‑balance limits from 35% to 25%; members flagged concerns about housing affordability, bond ratings and impacts on small towns.

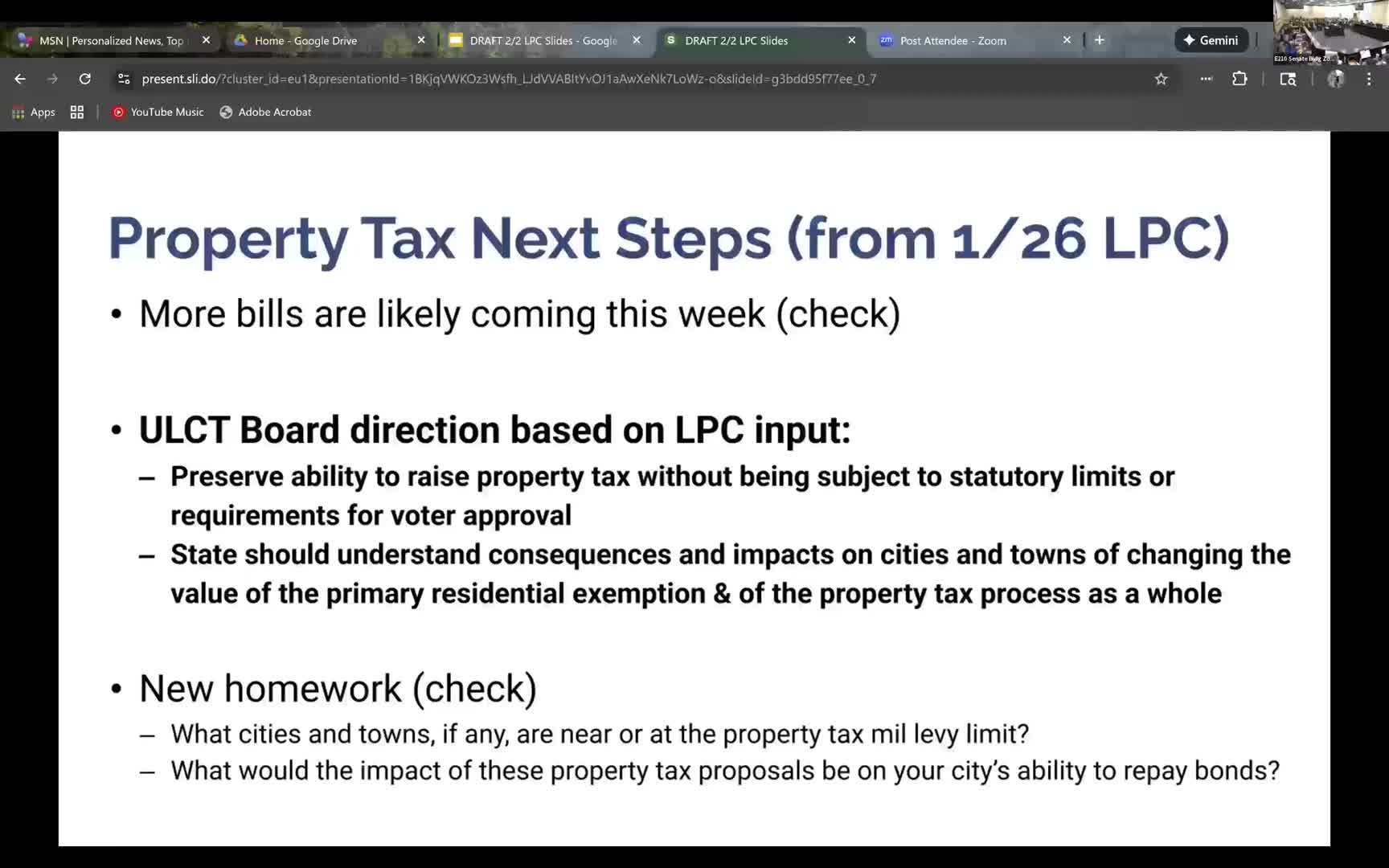

Cam, the League presenter, told members the first substitute to SB97 still includes a 5% cap on property-tax increases but said sponsors signaled that the cap may be removed in a later substitute. He described a change raising the definition threshold for 'new growth' so that improvements that increase a property’s value by less than 200% would be excluded from new‑growth calculations (the original threshold had been 100%).

Cam said the substitute would also reduce the permissible city general‑fund balance from 35% to 25% and would create a rebuttable presumption limiting the residential exemption for owners of many units (for example, an owner of 30 homes would be presumed not to qualify). He asked members for Slido feedback on those provisions and other concepts in the sub.

Members responded with detailed concerns. Gary Hill (Bountiful City) warned that tying reserve rules to tax‑increase authority and conflating reserve funds with ongoing operating revenue could create difficulties if voters refer tax measures, saying, "We now know through some litigation that it’s considered referable." Seth (a member who asked questions during the Slido polling) raised bond‑market implications and whether lowering reserve targets could harm municipal credit ratings; Cam acknowledged those concerns and said bond counsel arguments have been influential in prior conversations about caps.

Other members noted housing‑affordability trade‑offs. One attendee observed that shifting taxation from institutional owners to tenants or users could increase costs for renters and would not by itself improve affordability. Cam and others also discussed the bill’s draft language on short‑term rentals and how it could affect eligibility for the residential exemption.

The League asked members to provide follow‑up technical feedback (budget offices, bond counsel, or finance staff) so the League can summarize municipal concerns for sponsors. The presentation also reminded attendees of related measures under consideration, including House Bill 236 (required preliminary property‑tax meetings and a tentative operating budget notice) and House Bill 449 (a TABOR‑style voter‑approval/refund mechanism). Cam said the League remains 'position pending' on many private‑tax bills while it compiles member input.

Next steps: the League requested members return technical responses by the stated deadline and indicated it will relay Slido results and member feedback to legislators as bills evolve. The committee did not take any formal legislative positions during this meeting.