Oldsmar warns state property-tax proposals could cut city revenues by millions; council weighs fire assessment, service cuts

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

City staff told the Oldsmar City Council that several pending state constitutional amendments could reduce city ad valorem revenue by an estimated $2.7 million under one scenario and urged the council to consider a mix of fee adjustments, special assessments and measured service reductions to protect core services.

City staff told the Oldsmar City Council on Jan. 27 that a package of proposed state constitutional amendments could noticeably shrink the city's general fund and force difficult budget choices.

"If HJR 201 passes as currently drafted, you are looking at a reduction of about $2.7 million starting in fiscal 2028," Garrett Zieluf, the assistant administrative services director, said during a demonstration of the Pinellas County property‑appraiser dataset. Staff showed the tool to illustrate how different ballot scenarios would affect Oldsmar's roughly $7.8 million in ad valorem revenue.

The fiscal context matters: Finance staff presented unaudited FY2025 general fund figures showing total program expenditures of about $18.2 million and program revenues of roughly $3.5 million, leaving net general fund program costs of about $14.7 million that are covered by unrestricted revenues such as property taxes and utility taxes, Cindy Minow, a finance presenter, said. A one‑time land sale at the Odeon site added $2.25 million to capital and reserves but is not available for ongoing services.

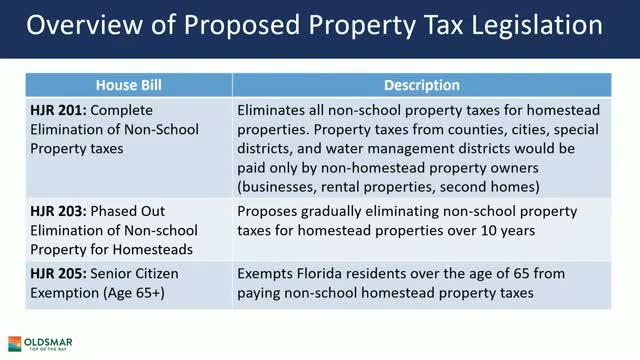

Why it matters: Several of the proposed measures would change who pays non‑school property taxes or change assessment caps. Minow summarized measures being debated in Tallahassee, including HJR 201 (exempting many homestead properties from non‑school ad valorem taxes), phased options such as HJR 203, senior exemptions in HJR 205, and SJR 550 (eliminating tangible personal property taxes). "Timing matters," she said, because measures that become ballot questions in 2026 would affect the Jan. 1, 2027 valuation used in revenue estimates for the FY2028 budget.

Council discussion focused on options staff recommends to manage revenue risk: Option A — targeted service reductions (library hours, temporary recreation‑center closures, postponing events or some capital projects); Option B — revenue optimization through fees and special assessments (including a potential fire assessment); Option C — a combination of the two; and Option D — take no action and wait. City Manager Felicia Donnelly told the council the meeting was intended to establish policy direction and help staff scope studies and community engagement, not to adopt final measures.

On special assessments: Donnelly and staff outlined the procedural and legal complexity of putting a fire assessment in place, including the need to retain a consultant, conduct cost‑of‑service studies and follow procurement rules. "If you chose to start soon, then we would be looking at a year from now," Donnelly said, describing how long a consultant‑led assessment process typically takes before revenue is realized in the budget.

Distributional and local impacts: Staff emphasized Oldsmar's unusual tax base mix — roughly half residential and half commercial — and said repealing tangible personal property (TPP) taxes would disproportionately hit Oldsmar relative to many Florida cities. "That $1 million hit for elimination of tangible personal property tax is significant for us," staff said, noting that one company's equipment divestiture had suppressed the city’s assessed growth the prior year.

Next steps: Council members signaled a preference for a blended approach (Option C) and directed staff to return with more detailed cost estimates, legal and procedural steps for any proposed assessments, and community‑engagement plans. Staff said a follow‑up item is expected at the council's second meeting in February.

There were no binding budget votes at the session; the meeting closed after a motion to adjourn.