District consultant: $33 million OPEB liability and trust could ease rising retiree health costs

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

An actuarial consultant told the finance subcommittee the district's total OPEB liability is about $33.1 million (measurement date 6/30/2024) and recommended considering an irrevocable OPEB trust and plan-design changes to slow future cost growth.

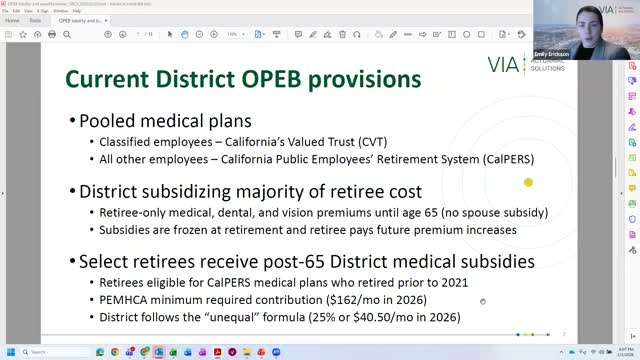

A consultant advising the district said its liability for other post-employment benefits, or OPEB, totaled about $33.1 million as of the June 30, 2024, valuation and that most of that cost is tied to pre-65 retiree medical subsidies.

Emily Erickson, a consulting actuary with Via Actuarial Solutions, told the Board Finance Subcommittee on Feb. 2 that projected premium subsidies for retirees start near $1.3 million for the current fiscal year and could rise toward $4 million over the next 30 years if current benefit rules and health-cost trends hold. "These costs are tied to health care premiums, which have been increasing," Erickson said.

The valuation separates an "explicit subsidy"—the portion of retiree premiums the district actually pays—from an "implicit subsidy" that GASB accounting requires the district to measure because retirees and active employees share the same medical plans. Erickson said the explicit subsidy accounted for roughly $22.5 million of the liability and the implicit subsidy about $10.6 million, together making the reported $33.1 million total.

Why it matters: the explicit subsidy represents cash the district must pay now and in future years; the implicit subsidy affects financial-statement liability under GASB standards. Erickson said the district currently finances retiree premium payments from general fund resources and has not set up a dedicated OPEB trust.

Options discussed: Erickson outlined two main approaches trustees can consider. Plan-design changes could reduce future district costs (for example, lowering the percentage of the single premium the district pays at retirement, setting a premium cap, or moving to a defined contribution approach). Any change to benefits, she said, will be constrained by collective-bargaining agreements and legal requirements tied to CalPERS medical plans.

The other approach is prefunding through an irrevocable OPEB trust. Erickson said an example using a 30-year horizon and a 6.25% assumed investment return shows prefunding can substantially shift the share of future payments covered by investment earnings. "If you establish an OPEB trust and build it up to $10 million, your net OPEB liability on the financial statements could drop from $33 million to about $23 million," she said.

Trust logistics and trade-offs: Trustees and staff asked about timeline and costs. Erickson said a trust can be established relatively quickly (some public trusts allow setup without an initial deposit), but accumulating meaningful assets requires identifying sustainable funding sources; contributions to a trust would be in addition to current pay-as-you-go premium payments. She pointed to options school districts commonly use in California, including CalPERS' CERBT-like public-trust options and PARS offerings.

Next steps: Trustees signaled interest in exploring a trust and asked staff to return with options, sample funding policies and risk-tolerance scenarios. The consultant offered to model contribution scenarios and review draft policy documents.

The presentation and discussion closed without a formal vote; trustees requested follow-up information for future contract negotiations and budget planning.