Get Full Government Meeting Transcripts, Videos, & Alerts Forever!

OCA’s first HPD analysis: utilization fell while commercial medical spending rose; staff to probe prices and intensity

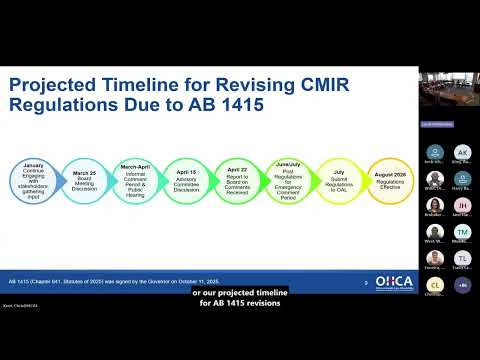

Summary

OCA used HCAI’s Health Plan Data (HPD) to compare 2022–23 commercial payer trends and found average utilization (share of members with any medical claim) declined while total medical expense per member rose, suggesting price or intensity changes may be driving spending growth; staff plan deeper HPD analyses on intensity and price variation.

OCA researchers presented an initial analysis using the Health Plan Data (HPD) to probe why commercial market medical expense per member rose in 2023 despite falling utilization.

Andrew Fair, research and analysis group manager, summarized a crosswalk between OCA’s aggregated submissions and the HPD and explained the analytic approach: converting HPD claims into a collapsed member‑payer‑year view and measuring three candidate drivers — average age, utilization (the share of members with at least one medical claim), and…

Already have an account? Log in

Subscribe to keep reading

Unlock the rest of this article — and every article on Citizen Portal.

- Unlimited articles

- AI-powered breakdowns of topics, speakers, decisions, and budgets

- Instant alerts when your location has a new meeting

- Follow topics and more locations

- 1,000 AI Insights / month, plus AI Chat