Get Full Government Meeting Transcripts, Videos, & Alerts Forever!

Powhatan County reviews FY27 budget scenarios and a 50/50 revenue-split proposal with schools

Summary

At a Feb. 12 budget workshop, Powhatan County staff outlined three tax-rate scenarios (75¢, 77¢, 79¢), proposed splitting community-impacting tax revenues 50/50 with schools, and showed how each scenario affects county revenue, positions, and CIP funding; no formal votes were taken.

Powhatan County officials on Feb. 12 reviewed fiscal year 2027 budget scenarios and a staff proposal to split community-impacting tax revenues evenly with the school division.

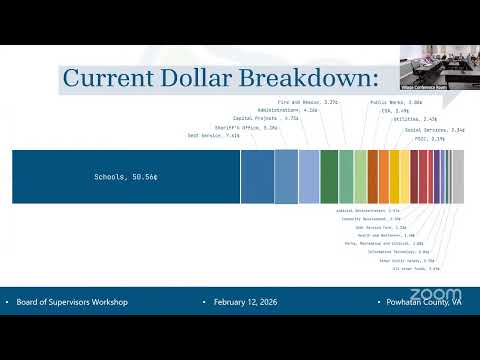

County staff opened the workshop with an overview of themes and values guiding the FY27 plan, saying cost growth is outpacing natural revenue growth and that the county must prioritize compensation adjustments, align the capital-improvement program (CIP) with affordability and borrow more sparingly for routine maintenance. Staff identified three real-estate tax scenarios — 75¢, 77¢ and 79¢ — and described the projected revenue, transfers to schools and net county revenue for each.

Under staff projections presented at the meeting, a 75¢ real-estate tax rate would produce limited additional resources but balance the budget while funding a modest set of personnel requests (a comp-and-class adjustment, a 3% raise line, select positions such as a public information officer and a few offset positions). At 77¢, staff said the county could fund additional items (including three full-time EMS staff) and…

Already have an account? Log in

Subscribe to keep reading

Unlock the rest of this article — and every article on Citizen Portal.

- Unlimited articles

- AI-powered breakdowns of topics, speakers, decisions, and budgets

- Instant alerts when your location has a new meeting

- Follow topics and more locations

- 1,000 AI Insights / month, plus AI Chat