Cheltenham finance committee flags $5.8M preliminary budget gap for 2026–27; options include fund balance, cuts or limited tax increase

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

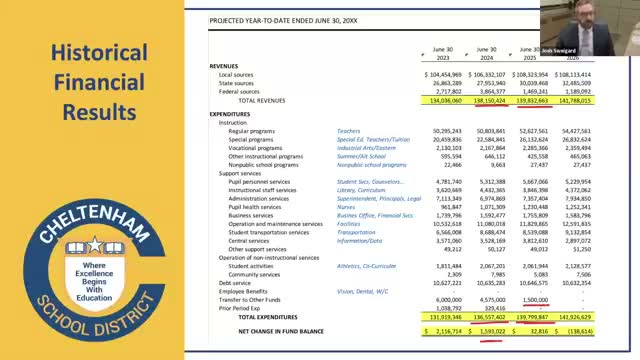

Administration presented a preliminary 2026–27 budget projecting a $5.8 million gap driven by a 22% health-insurance spike and lower real-estate assessment revenue; the committee discussed using fund balance, expenditure reductions and constrained tax capacity under Act 1.

Administration told the finance committee that preliminary numbers for the 2026–27 school year show total projected expenditures of about $146.7 million against projected revenues of roughly $140.0 million, leaving a roughly $5.8 million shortfall.

"We have a $5,800,000 gap to fill somewhere along the line between now and the end of the school year," said the administration presenter. He noted the projection does not include a tax increase and said the gap could be covered by a mix of tax increases, reductions, or use of fund balance.

Administration identified several drivers of the shortfall: a projected approximately $1.6 million decrease in real-estate-tax revenue tied to assessment changes and commercial tax appeals, and a large jump in health-insurance premiums. "The biggest factors driving that increase are wages and benefits, with the largest ... being our health insurance premium increase of 22%, which is roughly a $2,000,000 increase," the presenter said.

Special education tuition was called out separately: the administration said recent growth in out-of-district placements and limited private-school seats is shifting costs to the district and raising special-education tuition spending.

Board members pressed for clarity on how much of the shortfall is structural. Board member Daniel Schultz summarized the drivers and urged caution about relying on reserves: "It is not sustainable to pay for ... balance a budget using cash, using capital reserves," he said, and called for a multiyear plan to right-size recurring revenues and expenses.

Committee members also discussed statutory constraints on raising taxes. Administration noted the district's Act 1 index and tax-limit rules, observing that a full $5.8 million covered only by taxes would represent roughly a 6.47% increase in the tax levy, while the district's Act 1 cap is about 3.5% (and projected base indexes of roughly 3.1–3.2 percent in coming years), limiting the practical amount that can be raised without exceptions.

Administration said it is considering a combination of approaches: targeted expenditure reductions, negotiating on contracts or benefits, drawing from fund balance as a one-time measure, and pursuing state grant opportunities. Upcoming board agenda items include a planned resolution to apply for a state capital improvement grant that administration suggested could be timed to help with capital needs rather than recurring operations.

The committee did not adopt a final solution at the meeting; administration will refine the budget, present proposals for closing the gap, and return to the board for action as required.