Officials credit Impact Aid closeouts, lower health claims and custodial savings for district's larger fund balance

Get AI-powered insights, summaries, and transcripts

Sign Up Free

Summary

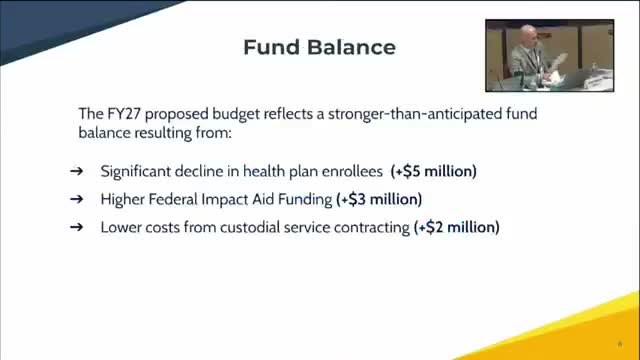

Administrators told the board that a combination of an Impact Aid closeout payment, a $5 million health-plan improvement and custodial contracting/vacancy savings explain a stronger-than-expected fund balance; they also explained stop-loss reimbursements and the difference between state and borough fund-balance calculations.

Board members spent substantial time probing why the district's fund balance grew more than expected and whether those gains are durable.

Chief Operations Officer Mister DeGraw said three main factors explain the increase: fewer enrollees in the district's self-funded health plan (which produced approximately $5 million in savings), higher federal Impact Aid receipts (administration raised its FY27 projection to just shy of $16 million), and contracting out custodial services (about $2 million in lower actual costs last year). DeGraw said the district also received stop-loss reimbursements when consultants processed large claims at fiscal year-end to secure reimbursements under the district's stop-loss coverage.

"What happened is we received a random closeout payment for a prior year," DeGraw said to explain Impact Aid volatility. He added that consultants and the district pushed large claims through in June so the stop-loss coverage (which he described as applying per claimant) would reimburse those expenses. "Once a claimant surpasses $500,000, it's a dollar-for-dollar reimbursement on that claimant's claims," he said.

Board members asked whether the risk-management (health-plan) fund can be used for operations. DeGraw said the district technically has access to that fund and that transfers historically were made from the general fund to the risk fund to pay claims; he also said the district does not routinely draw risk funds for operating purposes and that doing so would carry trade-offs.

Members pressed about the borough's fund-balance calculation. DeGraw explained the state calculation focuses on the general fund (10% of general fund expenditures with certain exclusions) and that the district is at the top end of the state-targeted range (about $20 million per the state calculation). By contrast, the borough's formula aggregates six funds — including the risk fund and equipment replacement fund — and counts year-end encumbrances differently, producing a higher aggregate number under borough rules.

Board members requested that staff prepare a slide showing a side-by-side comparison of the borough and state fund-balance calculations so the board and public can see what is and is not included under each method. DeGraw agreed to provide that comparison at a subsequent work session.

The administration cautioned that much of the revenue and claims data arrive with a delay and that Impact Aid closeouts and large claims are inherently difficult to predict; several board members urged caution about relying on one-time gains for ongoing operations.