Norwalk finance committee recommends 7% cap on FY27 operating budget after debate over health costs and reserves

Loading...

Summary

On Feb. 18 the Norwalk City Finance and Claims Committee voted 6–1 to recommend a 7% cap on the fiscal year 2026–27 operating budget to the Common Council after staff outlined large health-insurance and internal-service fund costs driving a roughly $21.96 million proposed increase.

The Norwalk City Finance and Claims Committee voted 6–1 on Feb. 18 to recommend a 7% cap on the fiscal year 2026–27 operating budget to the Common Council, after staff presented scenarios showing how the mayor’s proposal would translate into tax-bill changes across districts.

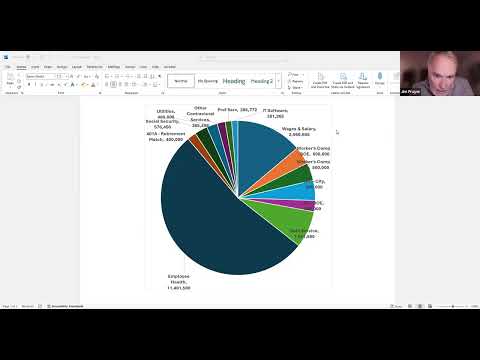

Finance staffer Jared told the committee that the proposed operating increases are driven largely by employee-health and other internal-service fund costs and contractual obligations. He said the internal-service fund balance that previously absorbed some health-cost growth has been drawn down and the city is now accounting for those charges in the operating budget. “The balance is no longer there in the internal service fund,” Jared said, describing the need to both cover rising costs and replenish the fund.

Jared quantified the scale of the increases: a total proposed operating increase of about $21.96 million, with roughly $11.4 million tied to employee-health expenses; he said about $7.0 million represents the flat increase and roughly $4.0 million is being added specifically to improve the net position of the internal-service fund. He also noted embedded headcount increases — roughly 10–11 positions in the fire department (two firefighters and the remainder supervisors/inspectors), two positions for a new recreation center and about 1.5 positions in grounds and facilities.

Committee members debated options for splitting the total cap between the city and the Board of Education (BOE). Jared presented three scenarios: the BOE full request, the mayor’s recommended split (4% for BOE, 10.72% for the city) and an incremental model that shows the tax impact of each tenth of a percentage point. The chair said those scenarios show how median district tax bills would change; Jared indicated a tenth-of-a-percent change would amount to about $12 in the sample district discussed.

Several members flagged the long-term structural risk of setting a higher spending baseline. “The difference between the full request and the proposed request appears modest,” said committee member Juan Lopez, “but the long‑term structural impact of setting a higher spending baseline raises a lot of questions.” Committee discussion touched on trade-offs including reserve replenishment, contractual obligations arising from recent union negotiations, and limited short-term savings from layoffs or early-retirement offers.

Committee members also discussed process: for FY27 the council will vote on a single percentage cap; charter changes will create separate cap votes for the city and BOE beginning in FY28. Members emphasized that the Board of Estimate and Taxation (BET) and the council will continue to review allocations and that adjustments later would require council action and a supermajority in some cases.

After the presentation and discussion, Roger (committee member) moved to vote on the mayor’s proposal and was seconded by Rich Dellinger. The committee approved recommending a 7% cap by a 6–1 vote; Nicole Eady cast the lone dissent. The chair said the recommendation will be forwarded to the Common Council at its next meeting.

The committee asked staff to provide the detailed spreadsheets and scenario tables used in the presentation and signaled follow-up questions on grant accounting (including a Perkins grant mentioned by a member) and the BOE’s treatment of new state aid.

Next steps: the Finance and Claims Committee’s recommended 7% cap will be presented to the Common Council for a vote at its upcoming meeting; additional review by the BET and reconciling steps could change allocations before a final tax levy is set.