Clark County reports first recorded general‑fund operating loss of $1.3 million in 2025; 2026 projection $16.5 million

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

Auditors told the council the general fund posted a roughly $1.3 million operating loss in 2025 — the first in the recent record — and projected a $16.5 million operating shortfall in 2026, driven in part by slow sales‑tax growth and inflation outpacing revenue.

Clark County's auditors reported on Feb. 25 that the general fund posted an operating loss of about $1.3 million in 2025 and that the county's preliminary projection for 2026 shows an operating loss of roughly $16.5 million, prompting councilors to discuss budget planning and fund‑balance strategies.

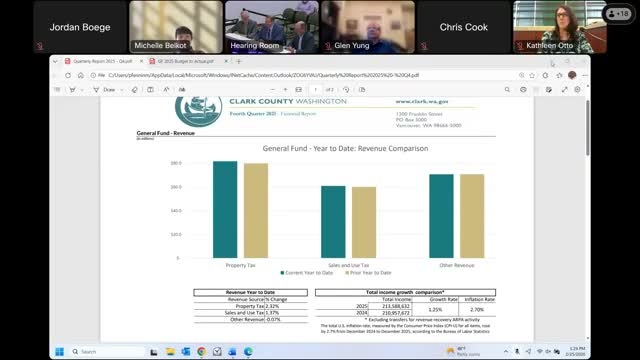

Mitchell Kelly, reporting-and-analysis manager in the auditor's financial services team, said property-tax revenue rose roughly 2 percent and sales-and-use tax grew 1.37 percent, but overall revenue growth for the general fund was about 1.25 percent — below the 2024–25 inflation rate of 2.7 percent (Bureau of Labor Statistics). "Our revenue growth was 1.25%" Kelly said, "and the inflation rate was 2.7% according to the Bureau of Labor Statistics," a gap that helps explain the operating shortfall.

At the same time, the county benefited from several expense savings (largely from vacancies): auditors reported about $7.2 million in unspent salary budget in 2025, and staff said some savings reflect positions that remain unfilled. But those savings were offset by weaker sales-tax performance (construction sector weakness was cited as the major contributor) and by one‑time or committed transfers — including ARPA commitments — that were moved to separate funds.

Mark Gassway, the county finance director, framed the problem as structural: "Our revenues are not growing at the same rate or slower than our expenses," he said, explaining the county's revised quarterly schedule to show structural deficit measures. Gassway noted that the general fund's projected 2026 operating loss will likely be covered in part by unassigned fund balance, which the auditors estimated at about $48 million of roughly $90 million in total fund balance at year end, but cautioned continued operating deficits could deplete one‑time reserves.

Auditors also flagged a notable insurance increase and other details: staff said liability insurance increased by about $481,000 (correcting an earlier figure of $281,000), and they described planned accounting and presentation changes to separate grants and managed transfers in future reports so the operating picture is clearer.

Councilors pressed staff on next steps. Councilor Belcott asked whether eliminating FTEs or reducing staff was being considered; auditors replied that staffing changes are a budget-cycle decision and recommended those conversations occur during upcoming budget planning rather than in a historical quarterly report. Councilor Young emphasized the importance of presenting inflation and revenue comparisons to the public to show long-term consequences for service delivery.

The presentation covered other funds as well: the road fund was close to budget, the public‑safety sales‑tax fund was near estimates, the community development fund had a cash-balance decline of about $1 million tied to lower development activity, and the mental‑health sales‑tax fund was projected at about $11.4 million after planned spend-down.

Next steps: staff said they will present more detailed, audited annual results in June and will return with budget‑planning materials and recommendations for how to address projected deficits in the 2026 budget process.