Ways & Means reviews bill to decouple Vermont tax code from federal changes, expand R&D and downtown credits

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

The Ways & Means discussion on Feb. 25 took up draft legislation to decouple Vermont tax law from several federal provisions, clarify apportionment rules for personal income tax, increase the state R&D credit to 75%, and raise the downtown/village tax credit cap from $3 million to $5 million; staff were asked to draft effective-date language and the committee recessed to resume work on a computing-cost adjustment.

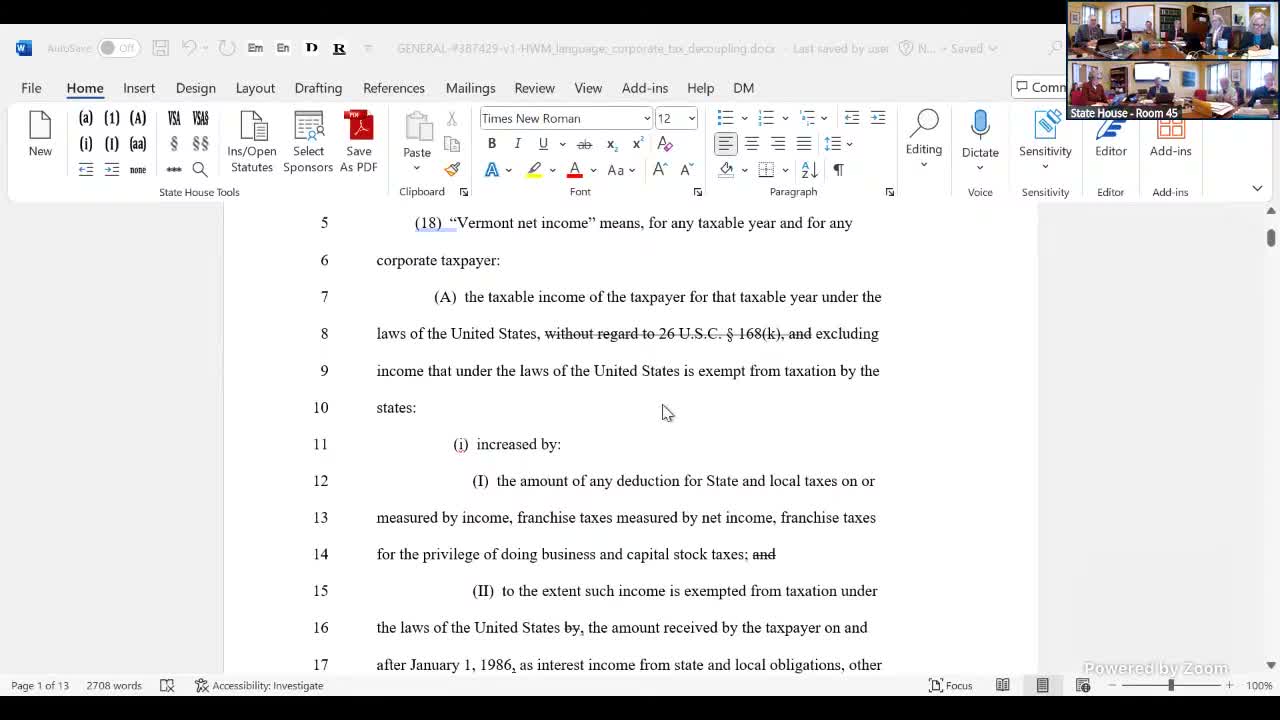

The Ways & Means panel discussed draft legislation on Feb. 25 that would decouple several Vermont tax provisions from recent federal changes and reshape a set of state credits and administrative rules.

Speaker 3, the presenter for the draft, told the committee the bill moves and clarifies existing language so Vermont’s tax administration will ‘‘treat property as if regular depreciation were used’’ rather than allowing the federal ‘‘bonus depreciation’’ treatment to reduce state taxable income. ‘‘What this is doing is it’s saying, we’re not gonna allow the bonus depreciation,’’ Speaker 3 said, explaining the draft also includes rules for sold or disposed property so taxpayers cannot deduct more than intended.

The draft would decouple Vermont from two bonus-depreciation provisions that were affected by the recent federal bill (HR 1), and add a decoupling from bonus depreciation for qualified production property, which covers certain machinery and production facilities. Speaker 3 said those changes are being moved and clarified in statute to reduce administrative interpretation burdens.

Committee members also discussed decoupling from the federal research-and-experimental deduction (sections 174/174A). Speaker 3 warned that federal changes to allow full expensing and that part of those changes were retroactive at the federal level could create immediate revenue effects in Vermont and complicate effective-date choices. The presenter summarized the bill’s tax-treatment approach for R&E expenses: expenses that are expensed federally would be added back for Vermont to preserve state revenue and focus incentives on in-state activity.

On the state research-and-development credit, Speaker 3 noted Vermont’s current credit is tied to the federal credit and limited to expenditures made in Vermont. The draft would expand the Vermont R&D credit rate (the discussion named moving the credit from 27% to 75%) and limit benefits to in-state expenditures. Speaker 1 observed that ‘‘by moving up to 75% … we would by far have the highest percentage in the country,’’ and committee members asked staff to post the statutorily required list of companies currently claiming the Vermont credit so members can review who benefits under current law.

The bill also proposes increasing the annual cap for the downtown and village center tax credit from $3,000,000 to $5,000,000 to direct more support toward local redevelopment projects. Speaker 3 said this shift is intended to reinvest some revenue saved by decoupling into targeted local development incentives. The presenter cited prior testimony from the Department of Community Development and the Preservation Trust in support of that element.

On personal income tax, Speaker 3 recommended changing statutory apportionment language. Under current law the apportionment for individuals looks at federal adjusted gross income (AGI) in a way that does not account for Vermont-specific additions and subtractions; the draft would modify the definition of AGI used for apportionment so that Vermont’s apportionment aligns with state taxable income.

Speaker 3 said the bill includes ‘‘link up’’ provisions tying Vermont to the rest of the federal tax code for 2025. The presenter noted effective-date language remains unresolved and recommended the committee consider language retroactive to Jan. 1, 2026, to manage the federal retroactivity and revenue impact questions.

Committee members raised competitiveness concerns and trade-offs. Speaker 2 asked whether removing some federal-based tax benefits would make Vermont less attractive to big businesses; Speaker 5 and others said the bill’s aim is to prevent loss of state revenue and to ensure credits reward investment in Vermont. Several members requested visual aids and additional data from the tax department to illustrate apportionment and the projected fiscal impact.

There were no formal motions or votes recorded in the transcript. Speaker 1 called for a brief recess and said the committee will return to consider a separate item, the cost-of-computing adjustment (H.8886), and that staff would draft and circulate proposed effective-date language for review.

Next steps: staff follow-up on effective dates, a posting of current R&D credit claimants as statutorily required, and further analysis from the Department of Taxes; the committee planned to resume work on the cost-of-computing adjustment at the next meeting.