Ithaca school board weighs tax-cap scenarios as officials outline preliminary 2026–27 budget

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

District leaders presented a preliminary 2026–27 budget projection and three budget-path options for the board to consider, highlighting a roughly 5% year‑over‑year cost increase, a 3.8% rise in state aid, and a calculated tax-cap of about 4.18 percent; staff will return with detailed expenditure scenarios.

At a Feb. 24 meeting, Ithaca City School District leaders presented a preliminary revenue and expenditure picture for the 2026–27 school year and asked the board for direction on tax‑levy scenarios and the use of fund balance.

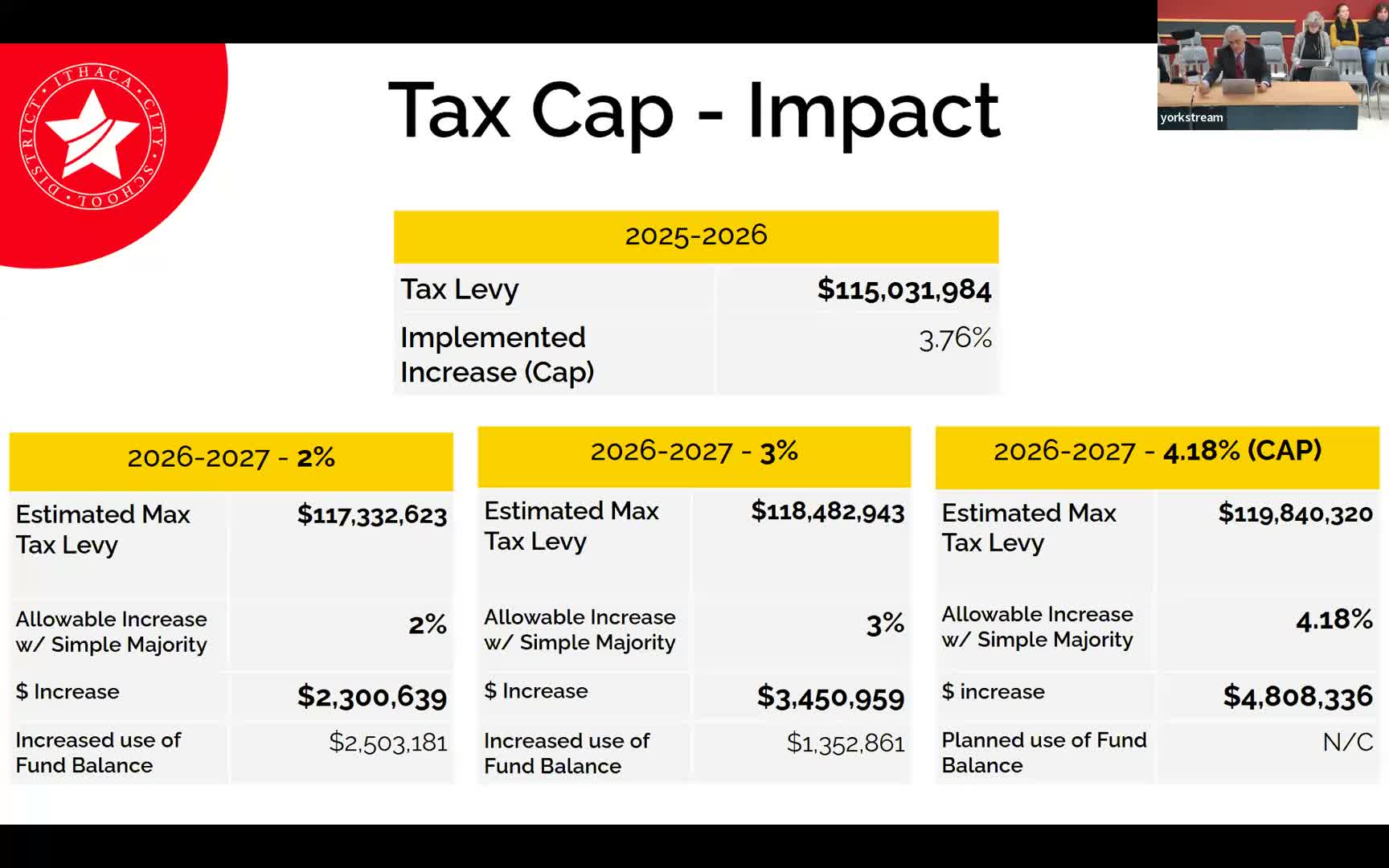

Superintendent Dr. Brown and district finance staff said the district’s initial projection for 2026–27 is preliminary and under active development. Finance staff described a year‑over‑year expense increase in the neighborhood of 5 percent and called out roughly $2 million in additional revenue from several sources. “The cap that was calculated is 4.18 percent,” the finance lead said, adding that the figure is the district’s working tax‑cap number for planning purposes.

The presenters told the board that the district’s revenue mix remains heavily dependent on local property taxes — about 70 percent — with roughly 25 percent from state aid and the remainder from other sources. Staff reported a state foundation aid increase of about 3.8 percent and noted miscellaneous revenue changes including a $55,000 increase from Cornell and an estimated $165,000 increase in other revenues.

Board members pressed for clarity about how much the district would need to draw on reserves under lower‑levy scenarios. Finance staff said if the district set a levy below the cap, it would need to draw on additional fund balance — for example, roughly $1.3 million at a 3 percent levy scenario and larger draws at a 2 percent scenario — and that going to the full calculated cap would eliminate the need for additional reserve use in the preliminary model.

“Going to the cap is something we said we would be recommending,” Dr. Brown said, framing the approach as one way to stabilize programing without immediate cuts. Board members debated the tradeoffs between preserving fund balance to protect bond rating and using reserves to limit taxpayer increases. Several trustees asked staff to present three concrete budget options at the next meetings that would: (1) assume the tax cap levy, (2) assume a lower levy with specified reserve use, and (3) assume additional spending reductions.

Staff emphasized that the figures presented were preliminary and that more detailed expenditure line items — including the distinction between mandated and discretionary costs and potential FTE (full‑time equivalent) changes — will be included in forthcoming materials. The board agreed to schedule deeper expenditure discussions in finance and facilities committee meetings over the next two to three months before a formal vote.

Next steps: district staff will return with three budget scenarios, a tax‑cap calculator demonstration, and detailed expenditure breakdowns to inform the board’s direction on the 2026–27 budget.