Charlottesville budget strains: transit staffing, collective bargaining and school requests drive revenue choices

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

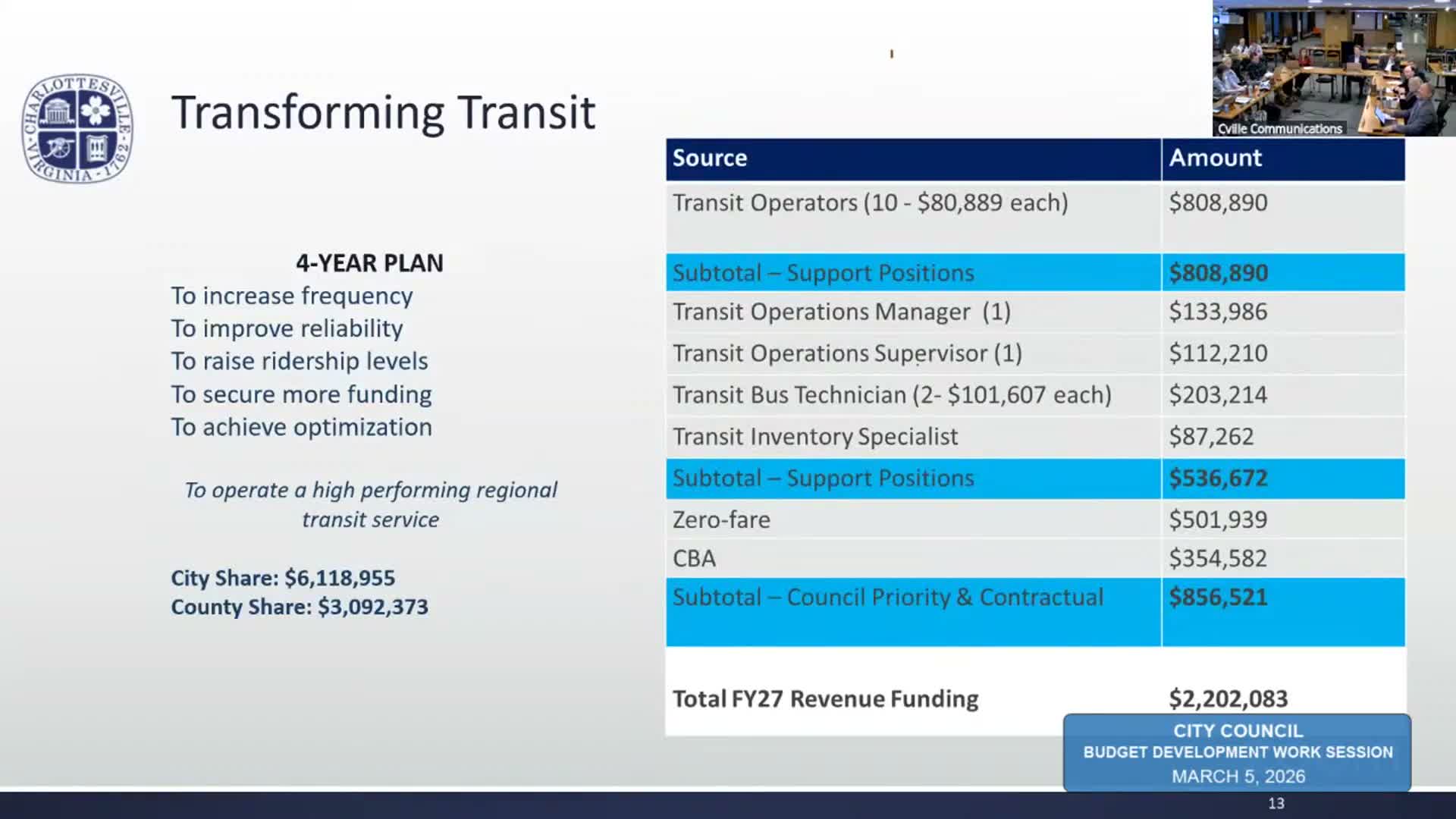

Staff told the council that transit expansions, collective‑bargaining costs and school funding increases are primary drivers behind the FY2027 shortfall; transit needs alone require new drivers and roughly $6.1 million in city share first‑year funding.

Charlottesville staff told councilors on March 5 that several recurring costs — notably transit expansion, collective‑bargaining impacts and increased school contributions — are the core drivers of FY2027’s revenue shortfall.

Transit staff (Presenter S8) described a four‑year plan to improve frequency, reliability and ridership. The presentation said the system needs roughly 106 drivers total (about 40 additional drivers) and associated supervisors and mechanics; the first‑year city share of the capital/operating plan was estimated at about $6.1 million and the county’s share at roughly $3 million. S8 said the initial identified funding gap to support bus operations, 0‑fare priorities and bargaining costs is about $2.2 million for year one.

On labor costs, staff said unaffiliated employees are budgeted for a roughly 2% step increase plus a pay‑scale adjustment, and collective‑bargaining settlements add an additional recurring cost. Staff quantified a collective‑bargaining impact of about $1.1 million in the draft budget.

School funding remains a major component of the spending side. Staff recapped that the school division’s original ask was about $6.4 million, was reduced through the process and the current draft funds $2.5 million to meet the most recent request; the CIP includes additional capital and maintenance funding for schools.

Council members and staff discussed tradeoffs: staff said that one‑time surplus can be used in limited circumstances but warned against using one‑time funds to cover recurring obligations because that risks future structural deficits and could affect bond ratings. Council asked staff to produce options that quantify what would be required to avoid such deficits if the council elects not to raise the real‑estate tax rate.

Next steps: staff will return with more granular options that illustrate the fiscal effect of specific levers (spending reductions, one‑time uses, or revenue alternatives).