Commission hears updated revenue forecast, staff warns $4M reallocation reduces capital available to about $26M

Loading...

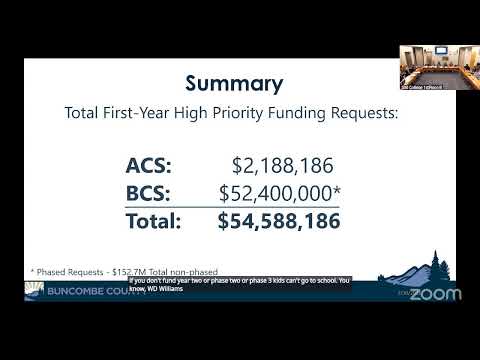

Summary

Officials reported an updated Article 39 sales-tax projection of $30.05 million for the fiscal year but said a prior $4.0 million reallocation to operating expenses will leave roughly $26 million available for school capital; staff previewed a $56 million share of a 2026 debt issuance that would add about $4 million in annual debt service starting FY27.

The School Capital Fund Commission on March 30 received an updated revenue and fund-balance report that showed estimated Article 39 sales-tax receipts of $30,050,000 for the fiscal year but clarified prior reallocations mean the commission will have substantially less capital to spend.

“We have estimated about a 6% year over year growth, and that is showing about 30,050,000.00 as our anticipated full revenue received for the end of the fiscal year,” Chair (speaker 2) said while presenting the revenue slide. Chair and staff clarified that because the board reallocated roughly $4,000,000 to school operating expenses earlier in the year, that amount will not appear in the capital fund and leaves approximately $26,000,000 available to the commission.

Finance staff (speaker 1) walked commissioners through the accounting treatment that affects how revenue is shown. “So there’s really 2 main types of accounting. There’s cash and then there’s accrual. And then in this government world, we do this thing called modified accrual,” the staff member said, explaining timing differences for sales-tax receipts and why the December collection is now reflected in the projection.

Commissioners also discussed expenditures and debt. Staff noted the commission typically spends $20–25 million a year on project activity (a recent year showed about $33 million) and identified 97 active projects, including about 15 nearing close-out. The county plans a 2026 debt issuance that would include roughly $56 million for school projects assigned to this commission; staff said that issuance would increase annual debt-service obligations by about $4 million beginning in FY27.

Members asked staff to return with a full fund-balance forecast at the next meeting that explicitly accounts for the $4 million reallocation, outstanding debt-service schedules that run through 2044, and scenarios for how the upcoming debt issuance will affect near-term and long-term cash flow. Staff agreed to provide those modeled scenarios at the April meeting.

No formal funding decisions were taken at the March meeting; the presentation and follow-up modeling will inform any future allocations or recommendations.