Tennessee Department of Revenue explains franchise and excise tax exemptions for insurance companies

Loading...

Summary

A Tennessee Department of Revenue presenter outlined which entities qualify for franchise and excise tax exemptions, how to register for the exemption, verification steps when not listed with the Secretary of State, and where to find statutory citations and contact resources.

An agency official with the Tennessee Department of Revenue on a recorded presentation explained the rules for franchise and excise tax exemptions that apply to insurance companies in Tennessee.

The presenter said the session "covers franchise and excise tax exemptions for insurance companies," and cited Tennessee Code Annotated section 67-4-2008 for exemption qualifications and section 56-1-102 for the statutory definition of an insurance company. The official defined an insurance company as including "all corporations, associations, partnerships, or individuals engaged as principals in the business of insurance."

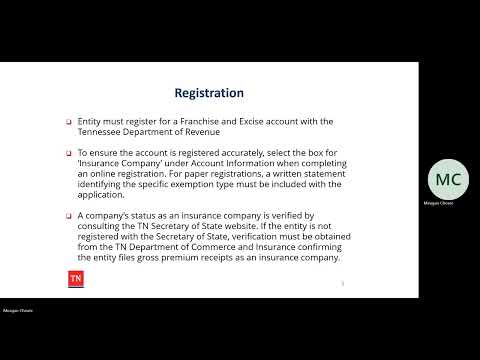

To qualify for the exemption, the agency official said the entity must register for a franchise and excise tax account with the Department of Revenue and select the insurance company option during online registration. For paper applications, the presenter instructed filers to include a written statement identifying the specific exemption type as "insurance company."

The presenter described verification steps: if an entity is not registered with the Tennessee Secretary of State, the Department of Commerce and Insurance must confirm that the entity files gross premium receipts as an insurance company before the exemption can be applied. "A company's status as an insurance company is verified by consulting the Tennessee Secretary of State website," the presenter said.

The official clarified the tax treatment: "Insurance companies are not required to file franchise and excise tax once they obtain their exemption because they pay gross premium tax with the Tennessee Department of Commerce and Insurance," citing Tennessee Code Annotated section 67-4-2009. The presenter contrasted that treatment with insurance agencies, noting that agencies are required to file Tennessee's franchise and excise tax.

For more information, viewers were directed to Tennessee Code Annotated sections 67-4-2008 and 56-1-102 and to the franchise and excise tax manual available on the Department's website at tn.gov/revenue. Contact options given included revenue.support@tn.gov and phone lines for general and franchise/excise tax questions.

The presentation closed with a reminder that a supplemental PDF is available in the webinar video library and with contact hours and phone numbers for further assistance.