Riverside board debates November income-tax proposal, $120 million campus as deficit warnings mount

Loading...

Summary

Leaders urged trustees to consider a 1% earned-income tax to support operations and a proposed $120M 7–12 campus; trustees split on packaging operations and facilities together, citing timeline, equity and partner commitments; board moved to executive session 5–0.

District leaders presented trustees with finance modeling and a campus plan during a work session that emphasized an urgent need for new revenue to avoid deeper deficits and potential state oversight.

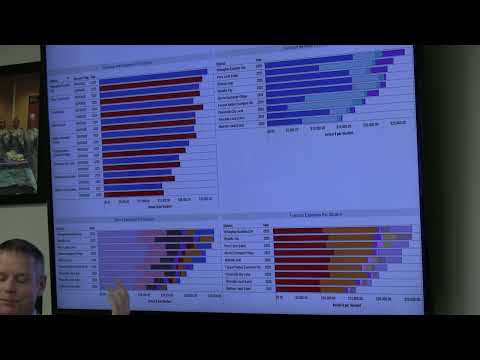

The district’s fiscal officer told the board the February forecast shows sustained multi-year deficit spending and said the district risks state fiscal watch if deficits exceed 8% of the general fund and fiscal emergency at 15%. "You can see we’re in deficit spending at $8.96 million," the fiscal officer said, describing the forecasted trajectory and the potential consequences for district operations.

Staff presented funding scenarios: a 4-mill property levy would raise about $6.9 million annually and a 5-mill levy about $8.6 million based on the transcript’s modeling; presenters cautioned that recent state property-tax rules (discussed as House Bill 920 in the presentation) constrain growth from property-based measures. In contrast, staff said a 1% earned-income tax was modeled to produce approximately $13.7 million annually, though income-tax collections have a multi-year ramp-up and would not fully appear until two years after approval.

On facilities, presenters showed preliminary renderings for a reimagined 7–12 Riverside campus and said a new-build and a hybrid renovation-plus-addition both landed in the same general cost envelope. The presentation gave a ballpark all-in cost near $120 million after contingencies and inflation — a figure leaders said is approximate and subject to refinement.

Trustees debated whether to ask voters for operating money and facilities in one combined question or to pursue only an operational levy this November and return later for a capital measure. Some trustees favored packaging to present a unified vision and avoid asking voters twice; others said a bond or separate levy limits the use of funds to capital work and protects building dollars from operational needs.

Board members raised constituent concerns about equity and timing. Several trustees said seniors and residents on fixed incomes express worry about tax changes, while staff noted the presented earned-income option would not apply to Social Security, pensions or retirement income per the presentation. Trustees also asked staff whether one-time reserves could cover maintenance needs; staff said about $1.1 million of a $3.0 million PI fund is restricted and roughly $1.82 million is available for repairs, but emphasized preserving reserves for catastrophic events.

An outside advisor recommended moving promptly on operational funding to stabilize the district. Staff and the advisor urged forming a levy committee, pursuing memoranda of understanding (MOUs) with potential partners such as the YMCA and neighboring jurisdictions, and compiling more detailed line-item financial scenarios before certifying any ballot measure.

The trustees did not approve ballot language at the meeting. They voted unanimously, 5–0, to adjourn to executive session at 7:52 p.m. to discuss personnel matters. The board instructed staff to continue refining the financial models, to pursue partner MOUs and to prepare campaign-level materials only if the board later authorizes moving forward publicly.

Next steps identified by staff: pursue MOUs with potential partners, assemble a levy committee to coordinate outreach and present updated, line-item financial scenarios and phased project options back to the board prior to any vote to place a question on the ballot.