Lifetime Citizen Portal Access — AI Briefings, Alerts & Unlimited Follows

Finance committee faces $2.6M fund‑balance draw for 2026–27 draft budget as prescription costs surge

Loading...

Summary

The proposed 2026–27 general fund budget would spend about $107.6M and rely on roughly $2.6M of fund balance to close the gap; trustees and residents pressed administration about rising prescription costs (noted as a 39.2% increase) and the sustainability of using reserves versus tax options.

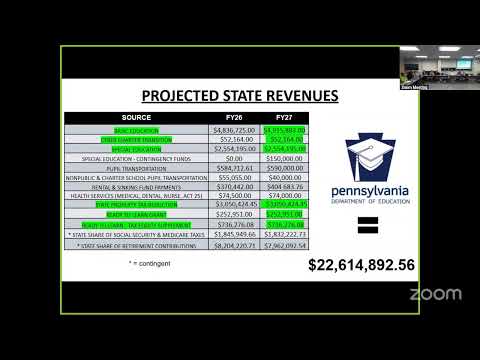

The finance committee reviewed a draft 2026–27 general fund budget that totals about $107.6 million and, as presented by business‑office staff, would require a draw of approximately $2.6 million from the district’s fund balance to balance revenues and expenditures.

Business‑office presenters attributed the shortfall to a combination of factors: personnel and benefit changes following the reorganization, a projected rise in medical and prescription expenses (the presentation cited a 39.2% increase in prescription costs), insurance premium changes and planned capital spending that includes a $40 million borrowing request tied to the district’s capital plan. "This budget balances by utilizing a little over $2,600,000 in fund balance," the presenter said during the meeting.

Why it matters: trustees and members of the public expressed concern that continued reliance on fund balance is not sustainable. Board members and residents pressed for clearer scenarios — including what a full allowable tax increase would yield, which parts of the capital plan could be phased or deferred, and how vacancies and retirements will be handled before positions are refilled.

Key budget details and drivers: business‑office staff explained personnel reorganization savings and noted offsets such as savings from procurement. They also highlighted several one‑time or variable items: $207,000 in previously approved food‑service equipment purchases, a $1.4M balance in a restricted medical‑access account, and contingency planning around inflation and bid alternates for capital projects. Procurement staff said recent RFP negotiations and vendor selections have produced savings of more than $400,000 across several services.

Board and public reaction: several trustees emphasized the need to reduce structural reliance on fund balance and asked staff to identify recurring savings and revenue options. Residents asked whether larger tax increases or referendums would be necessary; administrators said the board will present more refined options at the May meeting and is actively reviewing vacancies to determine whether positions must be backfilled.

Next steps: staff will return to the finance committee on May 19 with the final proposed general fund budget and any contract awards; trustees signaled they will continue to weigh capital timing, prescription‑cost mitigation and potential revenue options before final adoption.

Provenance: transcript segments from the finance call to order through the budget presentation and public Q&A.