Get AI Briefings, Transcripts & Alerts on Local & National Government Meetings — Forever.

Auditor‑Controller cites Workday progress, asks for internal audit capacity

Loading...

Summary

Auditor‑Controller and county fiscal staff said Nevada County implemented Phase I of a new Workday ERP on time and on budget and outlined Phase II (payroll/HR) scheduled for January 2027; the office asked the board to consider reinstating an internal audit position and funding to stabilize ERP operations.

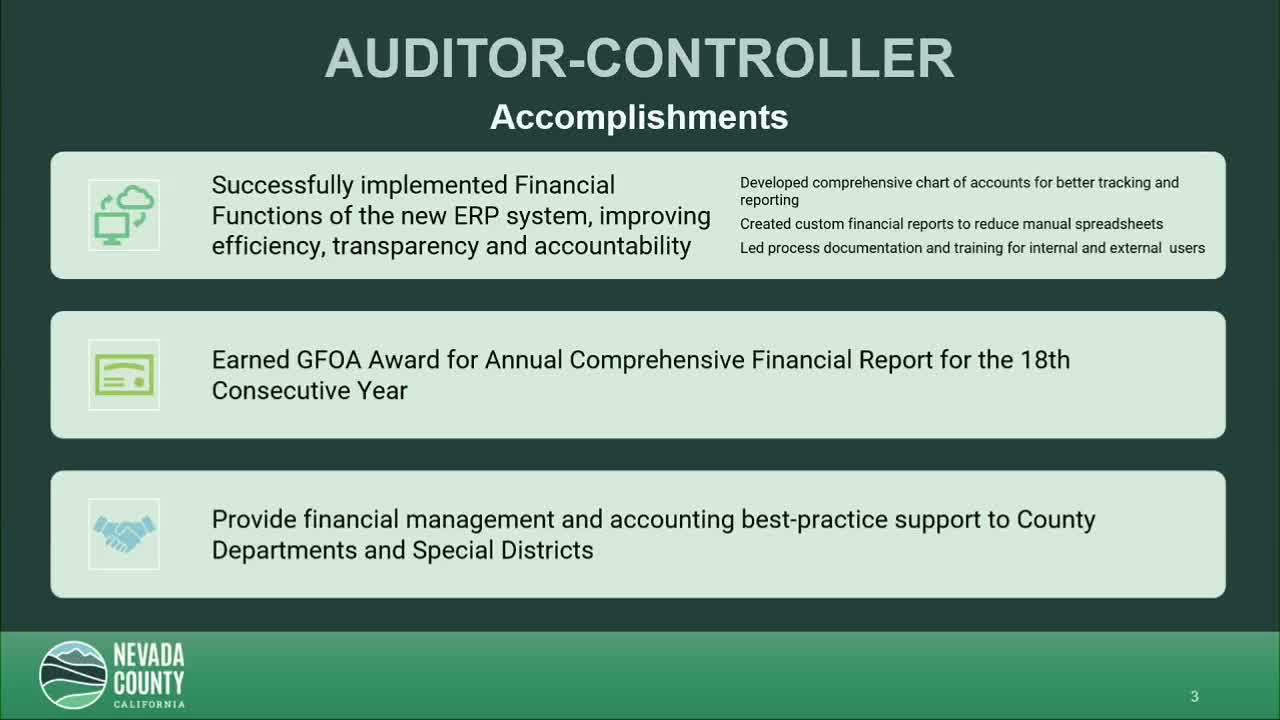

Gina (Auditor‑Controller) told the Board the office closed FY2024–25 with an award‑winning comprehensive financial report and successfully launched Phase I of the county's new enterprise resource planning system (Workday). She said the project replaced a system used for more than 20 years and delivered custom reporting and a new chart of accounts.

Gina said Phase II will focus on human‑resources and payroll functions and is targeted for a January 2027 go‑live. She described required parallel testing and additional staffing to validate payroll and benefits administration prior to full implementation. The office plans a permanent ERP support structure for user security, accounting structure maintenance and quarterly mandatory upgrades.

The Auditor‑Controller noted limited discretionary funding in the office and that personnel costs are the largest budget driver; the office requested reinstatement of a dedicated internal‑audit position that had been eliminated during the Great Recession. Several supervisors questioned whether ERP efficiencies would reduce staffing over time; Gina and Deputy CEO Erin Mettler said potential savings will likely be seen in other departments and that staffing needs remain driven by transaction volumes.

Supervisors asked for a later analysis showing how ERP investments translate into operational savings; board members also discussed long‑term costs for Workday maintenance and recent increases in intra‑fund charges that affected the office's operating budget.

The board left the issue open for further review in the budget subcommittee and asked staff to return with cost‑benefit detail and options for funding a potential internal audit position.