Get Full Government Meeting Transcripts, Videos, & Alerts Forever!

Tennessee Department of Revenue outlines franchise and excise tax exemption rules for investment entities

Summary

The Tennessee Department of Revenue explained eligibility and filing rules for franchise and excise tax exemptions for certain investment entities under Tennessee Code Annotated §67-4-2008, including 90% asset and income thresholds, required forms (FAE-183, FAE-170), filing deadlines, a $200 late-filing penalty, and contact resources.

Meagan Choate, Taxpayer Services Supervisor at the Tennessee Department of Revenue, presented a webinar explaining how certain investment funds may qualify for a Tennessee franchise and excise tax exemption.

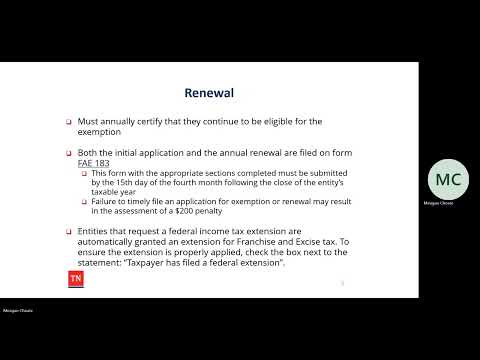

Choate said the exemption applies to entities that are "a limited liability company, a limited partnership, a limited liability partnership, or a business trust." She cited Tennessee Code Annotated §67-4-2008 as the governing statute. To qualify, she said, "at least 90% of the cost of the entity’s total assets must consist of qualifying investment securities, bank deposits, and office space and equipment,"…

Already have an account? Log in

Subscribe to keep reading

Unlock the rest of this article — and every article on Citizen Portal.

- Unlimited articles

- AI-powered breakdowns of topics, speakers, decisions, and budgets

- Instant alerts when your location has a new meeting

- Follow topics and more locations

- 1,000 AI Insights / month, plus AI Chat