Get Full Government Meeting Transcripts, Videos, & Alerts Forever!

Tennessee Revenue explains who qualifies for Obligated Member Entity election and filing steps

Summary

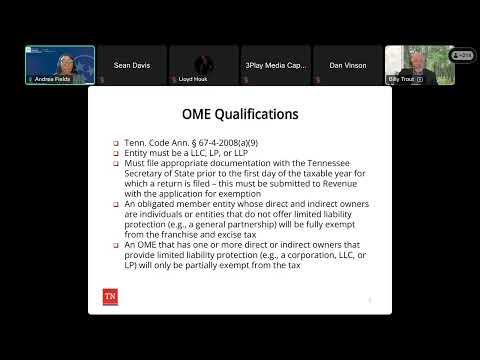

Tennessee Department of Revenue officials outlined how the Obligated Member Entity (OME) election can provide pass-through treatment for franchise and excise tax, detailed qualifying entity types (LLC, LP, LLP), required Secretary of State filings, key deadlines, and how the election affects limited liability.

Billy Trout, Taxpayer Education with the Tennessee Department of Revenue, opened a departmental webinar describing the Obligated Member Entity (OME) election as a way to obtain pass-through tax treatment for franchise and excise taxes.

"The purpose of this OME election-- it's to obtain a pass-through tax treatment," Trout said, adding that the election is intended to "avoid duplication of taxation" under Tennessee law.

Why it matters: The department said OME can prevent an entity and its members from being taxed twice at the entity level, but only certain business types and properly timed filings qualify. The session cited Tennessee Code Annotated 67-4-2008 as the statutory basis for the OME provisions.

Who can elect and how it works: Department officials said only limited liability companies (LLCs), limited partnerships (LPs), and limited liability partnerships (LLPs) may make the election. Trout said all members must make the election for it to be valid: "If one or more members doesn't make the election,…

Already have an account? Log in

Subscribe to keep reading

Unlock the rest of this article — and every article on Citizen Portal.

- Unlimited articles

- AI-powered breakdowns of topics, speakers, decisions, and budgets

- Instant alerts when your location has a new meeting

- Follow topics and more locations

- 1,000 AI Insights / month, plus AI Chat