Lifetime Citizen Portal Access — AI Briefings, Alerts & Unlimited Follows

Tennessee Revenue details consolidated net worth election, warns it is binding for five years

Loading...

Summary

Tennessee Department of Revenue staff explained who may use the voluntary consolidated net worth election for franchise and excise tax, how the election is calculated and filed (paper or TenTAP), common errors to avoid, and where taxpayers can get help.

Tennessee Department of Revenue staff used a taxpayer-education webinar to walk accountants and business owners through the consolidated net worth election for franchise and excise tax and urged care before electing because the choice is binding for five years.

"It's binding for 5 years," said Cameron Young of the department's audit division, summarizing a key constraint about the voluntary election and the reason taxpayers should model the group's likely net‑worth profile before opting in. The webinar, led by Katie Julian of taxpayer education with presentations from Andrea Fields (registration) and Billy Trout (manager, taxpayer education), ran about an hour and was recorded for the department's webinar library.

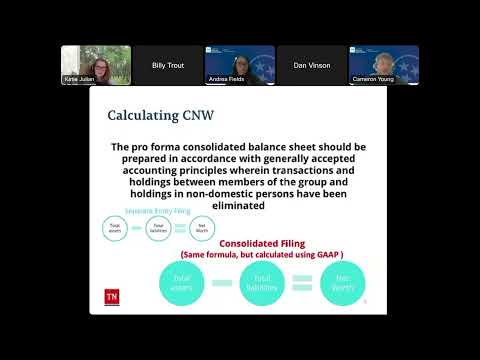

The panel defined the consolidated net worth election as an option that lets affiliated entities compute franchise-tax net worth on a consolidated basis for the net‑worth tax base only, rather than reporting each entity's net worth separately. "A consolidated election is not a combined return," Andrea Fields, a supervisor in registration, clarified, distinguishing the CNW election from unitary or combined filings used by some financial institutions.

How it works: net worth is calculated as total assets minus total liabilities; consolidated filings generally follow GAAP and use pro‑forma federal return eliminations to exclude items and members that don't meet the ownership or domestic‑person tests. Cameron Young said the process will exclude members without the required ownership threshold and non‑domestic persons that do not meet the domestic‑person test.

Who qualifies: an affiliated group includes entities in which the taxpayer directly or indirectly holds more than 50 percent ownership (upstream or downstream). Panelists stressed attention to the CNW form's Part 1 and Part 2: list Tennessee‑filing members on Part 1 and nonfiling affiliated members on Part 2 to avoid creating accounts in error. "We frequently see that error occur on the elections where entities that are not subject to franchise tax, they're listed on part 1, and accounts are created for those entities in error," Fields said.

Filing and timing: taxpayers may file the CNW election using a paper form or electronically via TenTAP (Additional Actions → consolidated net worth election registration). The election must be made on or before the due date of the return (including federally granted extensions) for the period the election first applies; late elections may be considered if filed before an extension due date or if the commissioner grants good cause, such as a natural disaster. Amended elections are required when members are added, sold or liquidated; departing members compute net worth unconsolidated (Schedule F‑1) while the group uses Schedule F‑2.

Practical points and common mistakes: the panel urged filers to ensure names and EINs match Secretary of State records and to include articles of amendment when names have changed; unsigned paper applications and missing account numbers are frequent grounds for denials. Katie Julian demonstrated the paper form and TenTAP workflow and advised filers to check the CNW checkbox on the return so the system applies Schedule F‑2 rather than F‑1.

Nexus and small businesses: the panel said out‑of‑state nexus depends on property, payroll and sales; registering with the Tennessee Secretary of State can create a $100 minimum filing obligation even when in‑state activity is minimal. "If you registered here at least with the secretary of state, it basically turned the machine on," Billy Trout said, explaining why some businesses that have little or no ongoing Tennessee activity nonetheless receive franchise and excise filing obligations.

Credits and unitary groups: Cameron Young explained credits generally cannot be transferred between separate taxpayers, though unitary filings for specific financial institutions or captive REITs may allow use of credits generated by subsidiaries under the unitary filing rules. Andrea Fields described how a unitary group (typically certain financial institutions) files a combined return for unitary members, which is distinct from the CNW election.

Resources and help: the department directed attendees to tn.gov/revenue (Taxpayer Education → Tax Webinars and Tax Manuals → Franchise and Excise Tax Manual) for recorded webinars, guidance and the CNW paper form. For follow up, email revenue.support@tn.gov (which opens a help ticket) or call the registration group at (615) 253-0700; the department's general tax line is (615) 253-0600.

The webinar closed with a reminder that CNW can be advantageous when group members have offsetting losses and gains, but that the five‑year minimum and record‑keeping requirements mean taxpayers and their advisers should evaluate the likely multi‑year impacts before electing. The department said the recording and PowerPoint will be posted in its webinar library.