Lifetime Citizen Portal Access — AI Briefings, Alerts & Unlimited Follows

OJP webinar outlines pass-through entity duties for overseeing subrecipients and responding to OIG findings

Loading...

Summary

The Office of Justice Programs reminded grant recipients they are responsible for oversight of subrecipients, detailed pre- and post-award risk assessments and monitoring steps, and highlighted OIG findings that motivated updated training and the release of an OJP toolkit.

Ira Holmes, Training and Policy Manager in the Office of the Chief Financial Officer at the Office of Justice Programs, led a webinar advising pass-through entities on their legal and programmatic obligations for overseeing subrecipients under Uniform Guidance.

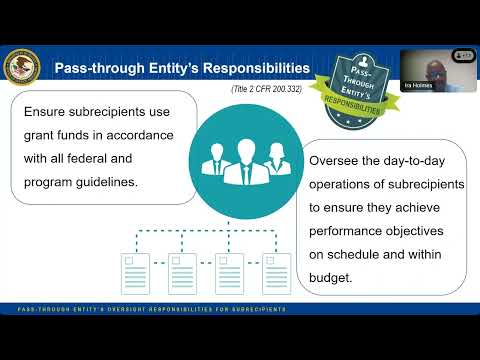

Holmes said pass-through entities — the primary non-federal grant recipients that make subawards to others — “must ensure that subrecipients use grant funds in accordance with all federal and program guidelines” and that entities oversee subrecipient operations enough to ensure performance objectives and reporting obligations are met. He cited provisions in Uniform Guidance (CFR 200) and specifically noted CFR 200.332 as the source for pass-through responsibilities.

The presentation distinguished subrecipients from contractors: Holmes said subrecipients typically have programmatic decision-making responsibilities, determine beneficiary eligibility, and are accountable for program outcomes, whereas contractors provide goods or services in the normal course of business and generally are not subject to program compliance requirements. “Substance takes precedent over form,” he said, urging grantees to evaluate the actual characteristics of the relationship rather than relying on labels.

Holmes walked attendees through required pre-award steps: written, documented policies and procedures that describe how subawards will be managed throughout the award lifecycle; publicly announcing funding opportunities and eligibility; checking SAM.gov for suspensions or debarments before awarding; and including award identification data elements such as the subrecipient’s UEI and the federal award identification number.

He recommended pre-award risk assessments that consider application quality, financial stability, past audit findings, and other indicators, and explained how those assessments can justify imposing additional, more restrictive terms and conditions on a subrecipient when necessary (so long as those conditions do not prevent the subrecipient from meeting program objectives).

On post-award oversight, Holmes described developing an annual monitoring plan that includes all subrecipients and uses a scoring system to set monitoring frequency and depth (low/medium/high). He said monitoring should verify that subrecipients have adequate internal controls, that claimed reimbursable costs are allowable and reasonable, and that any conflicts of interest are identified and documented. Holmes gave concrete site-visit best practices: send an advance notification letter listing requested documents, hold an entrance conference with appropriate subrecipient staff, review applications/agreements/drawdown histories/audit reports, and hold an exit conference that records unresolved deficiencies and a date-certain follow-up.

Holmes reviewed available remedies for noncompliance under Uniform Guidance, including imposing additional conditions, temporarily withholding funds, disallowing activities, suspending or terminating awards, and initiating suspension or debarment. He also summarized closeout timing: subrecipients should submit final financial and performance reports within 90 days of the end of their performance period and pass-through entities generally have 120 days to complete closeout activities.

Explaining why OJP offered the webinar, Holmes said Office of Inspector General reviews found many pass-through entities lacked written policies and procedures for subawards, had not implemented monitoring effectively, and had not budgeted sufficient funds or training for monitoring staff. He said those findings motivated the creation of an OJP toolkit and renewed training offerings.

Holmes pointed attendees to resources — Uniform Guidance (CFR 200), the DOJ Grants Financial Guide, OJP’s toolkit and website, the Comptroller General’s “Green Book” on internal control, and Treasury/COSO materials — and announced forthcoming in-person OJP financial-management training sessions, emphasizing that slides and toolkit links would be shared with participants.

During Q&A, participants pressed for clarifications. In response to a question about whether police overtime payments for attending training constitute a subaward or a contract, Holmes said those payments are not a procurement contract because the officers are not providing goods or services to the pass-through entity. On FFATA reporting (whether an overreported amount should be adjusted if the subrecipient spends less than reported), OJP staff said they would follow up with specific guidance. On sole-source procurements, Holmes said prior federal approval is required for noncompetitive awards when the procurement exceeds the simplified acquisition threshold (discussed as $250,000) and described the documentation needed for a sole-source justification through JustGrants.

Participants were told OJP staff can review subrecipient-monitoring policies and provide feedback during monitoring visits, and that tools/templates in the OJP toolkit and slide packet can be used to develop monitoring plans. Holmes closed by thanking attendees, confirming slides would be distributed, and reminding participants of an upcoming webinar on conference costs.

The session emphasized that pass-through entities retain responsibility for oversight regardless of whether funds are passed to third parties and recommended that entities document their determinations, risk assessments, and monitoring activities to address OIG concerns and meet Uniform Guidance requirements.