Lifetime Citizen Portal Access — AI Briefings, Alerts & Unlimited Follows

Issuers told how Type 3 and Type 5 multifamily conversions differ: who must act and when

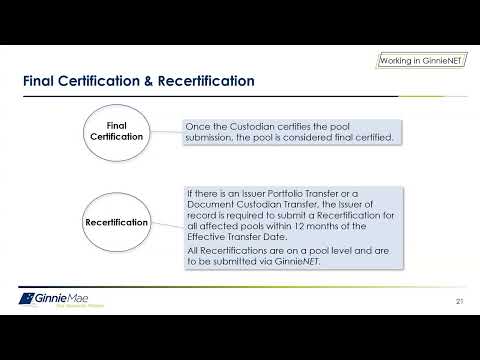

Loading...

Summary

Ginnie Mae trainers explained conversion methods: Type 3 requires investors to return CLC positions to the Fed before PN issuance; Type 5 is automated with the CLC canceled and PN issued three business days after final draw, and issuers should confirm holder proportions ahead of conversions.

Ginnie Mae presenters spent a substantial portion of a closed training session explaining differences between multifamily conversion methods and what issuers and investors must do for each.

Wade described a Type 3 conversion as the conventional or manual method: "the investor has to do a little bit of work," he said, explaining that investors must return all CLC positions to the Federal Reserve Bank of New York before a permanent loan (PN) pool can be delivered. Michelle Murphy, a customer-service subject-matter expert in the training, said Type 3 is used when there is no final draw or when collected principal is greater than the final draw, and that coordination among investors is required so a PN can be issued.

By contrast, trainers said Type 5 conversions are the more automated process issuers prefer. Michelle told attendees that for Type 5 "the final CLC is delivered for settlement, and 3 business day later, the CLC is automatically canceled when the PN is delivered through the Fed for settlement," meaning investors usually do not need to initiate returns for the CLCs in the same way as with Type 3. Both presenters stressed that issuers should confirm who holds positions and the proportions they hold before initiating a conversion so settlement and PN allocations are correct.

The trainers also noted operational guidance: monthly pool dates calendars establish the last day to submit a Type 5 conversion (typically six business days prior to a target, counting a day for mailroom/processing), and that conversions done on the last business day of a month may delay CUSIP/QSIP visibility until the next business day.

For issuers planning conversions, the presenters recommended checking guidance in the MFPDM user manual and consulting account executives or the Ginnie Mae customer support team if unusual circumstances arise.