Lifetime Citizen Portal Access — AI Briefings, Alerts & Unlimited Follows

Myers asks Lake County board to accept $700,000 sale price; supervisors continue appeal to April 21

Loading...

Summary

Myers Storage LLC appealed a 2023 reassessment after the county raised the property's value; the assessor defended a $1.21 million income-based valuation while the appellant presented the $700,000 purchase as market evidence. The board continued deliberations to April 21, 2026, and set a written-submission deadline of April 17.

The Lake County Board of Supervisors, sitting as the Board of Equalization, continued deliberations on an assessment appeal by Myers Storage LLC after hearing presentations from the assessor's office and the appellant.

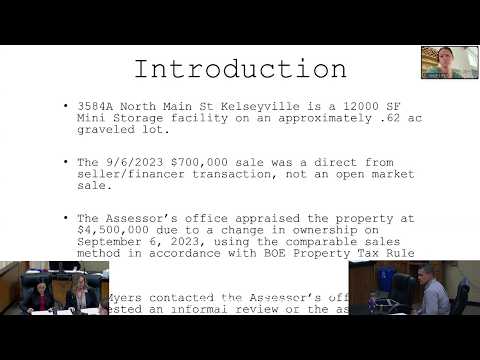

The assessor's office, represented by Landai Janakis and Michelle Bocchanani, presented three valuation approaches and said the income approach produced an indicated value of $1,210,000 for the 12,000-square-foot mini-storage facility at 34584A North Main Street in Kelseyville. "Using the income approach in accordance with BOE property tax rule 8, the assessor's office determined a value of $1,210,000," Bocchanani said as she reviewed comparable sales, cost estimates from Marshall and Swift guides, and a deed of trust recorded 09/06/2023.

The appellant, identified in the hearing as Myers, told the board he purchased the property in September 2023 for $700,000 and asked the board to accept the purchase price as the best evidence of market value. Myers described the facility as basic slab-on-grade construction with "no water, no paving, no electricity, no fencing, no lights, no cameras, no office, no fire sprinklers," and argued those limitations make the county's higher comparables and per-square-foot calculations inappropriate. "The $700,000 sale price is the best evidence of fair market value," Myers said, arguing the transaction was arm's-length and part of a 1031 exchange.

A witness for the appellant, Rob Brown, testified that private-sector appraisal practice and the property's limited infrastructure supported a lower valuation and criticized the county's comparable-sales set as not truly comparable. The assessor's presenter noted the office had used multiple approaches and defended the income approach as the most reliable indicator for an income-producing property.

Supervisors raised procedural questions after materials (binders) were distributed prior to the evidentiary portion. County Counsel advised the board that staff had confirmed that substantive contents of the binders were not reviewed by board members and that the Revenue and Taxation Code permits the board to deliberate in private after the evidentiary portion but that the board may choose open deliberations.

Given the volume of evidence and the need for careful review, County Counsel proposed, and the board adopted, a motion to continue the matter for deliberation in open session on April 21, 2026, at 1:00 p.m., and to direct both parties to submit any written arguments to the clerk of the board by the close of business on April 17, 2026. The motion passed on a 5-0 vote.

The Board of Equalization proceedings will resume on April 21, 2026, for open-session deliberations and possible findings of fact; until that time, the assessor's office and the appellant may submit the requested written materials that will be added to the record.