Get AI Briefings, Transcripts & Alerts on Local & National Government Meetings — Forever.

Lackawanna County officials, contractor explain reassessment process and timelines at public meeting

Loading...

Summary

Tyler Technologies and the county assessment office outlined how the upcoming countywide reassessment will be done, the 30‑month sales window used for valuation, the revenue‑neutral rule that prevents taxing bodies from collecting more in the reassessment year, and the timetable for informal reviews, formal appeals and final certification.

Tyler Technologies representatives and the Lackawanna County assessment director told residents at a public meeting that the countywide reassessment will reset the county's base year from 1968 to 2026, and that new assessed values will take effect for tax purposes Jan. 1, 2026.

Samantha Edwards, project manager for Tyler Technologies, described the reassessment method used in Pennsylvania, saying, "Base year is the year in which the last county wide reassessment occurred." She and Tyler colleague Tatum (Tate) Kreutz and Patrick Tobin, director of the county Assessment Office, explained the valuation steps, public review opportunities and the schedule residents should expect.

The reassessment uses a 30‑month sales period for market analysis, Edwards said, covering sales from Jan. 1, 2022, through June 30, 2024. Tyler's valuation team calibrated computerized models for market areas in the county and applied the cost, income and market approaches where appropriate. Edwards said tentative appraised‑value notices will be mailed to all property owners by the end of the month; recipients who disagree can schedule an informal review with a Tyler representative and, if still dissatisfied, pursue a formal appeal with the county.

Tatum Kreutz summarized common concerns residents raise about reassessments and addressed them directly. On taxes he said, "Will a reassessment mean that I will pay more in taxes? Not necessarily." He explained that Pennsylvania law requires reassessments to be revenue neutral: total countywide tax revenues for the taxing bodies cannot increase in the year the reassessment takes effect because millage rates will be adjusted to reflect higher total assessed value. Kreutz used a simple example to show that if assessed values double in aggregate the millage rate will be cut roughly in half for taxing bodies that keep the same budget.

Pat Tobin, director of the county Assessment Office, confirmed the county's current base year is 1968 and described the county's role in certification and tax roll publication. He said the county must certify final assessed values by Nov. 15, 2025, after informal reviews and formal appeals are complete, and that certified values will be posted and reflected in tax rolls for 2026. Tobin advised residents with immediate questions about current tax bills or penalties to contact the Assessment Office directly.

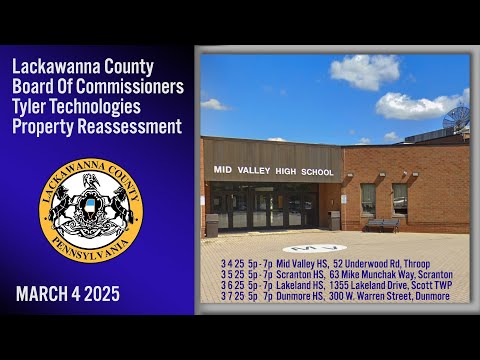

Tyler and county staff described the public process and opportunities for corrections: field data collectors recorded exterior measurements and visible improvements from May 2022 through December 2024; data mailers were sent to residential owners with improvements to confirm or correct recorded information; tentative value notices will follow; informal reviews will run next month through May; and final notices and certification will follow the appeals process. Kreutz described informal reviews as one‑on‑one meetings, in person or by phone, where evidence (MLS listings, appraisals within the 30‑month sales window, photos, permit records) may be submitted to correct the record.

Speakers repeatedly urged property owners to review data mailers and tentative value letters carefully and to bring documentation to informal reviews. Tobin and Edwards said certain items (for example, above‑ground portable sheds under 250 square feet) are not picked up as permanent improvements, while decks, enclosed porches and in‑ground pools are assessed. Edwards noted finished basement living area factors into value but is not counted as above‑grade living area for square‑foot reporting in Lackawanna County.

Residents asked about timing, how millage changes will affect individual tax bills, and whether the recent county tax increase is related to the reassessment. Tyler and Tobin answered that the reassessment does not change taxing bodies' budgets for the reassessment year and that the county commissioners' decision to raise taxes earlier in the year is separate from the reassessment process; Tobin said decisions about county or municipal budget changes must be directed to the commissioners or local councils.

Tyler estimated the full reassessment contract cost at roughly $5,000,000 and advised that more frequent reassessments (Edwards said every six years is preferable to the 58 years since the county's last full reassessment) would reduce cost and distributional shocks in the future. Kreutz and Edwards described quality‑control steps: repeated data collection, model calibration, and post‑mailing review to correct misrecords.

The meeting closed with an offer from Tyler and the Assessment Office to remain after the public session for one‑on‑one questions. Edwards provided her email in the presentation, and Tobin provided the Assessment Office phone number shown on meeting slides: (570) 963‑6728.

Ending: Residents will receive tentative value notices this month and can schedule informal reviews; final certified values will be set by the county following appeals and will be used for tax year 2026.